MikeyGen73

Growth prospects

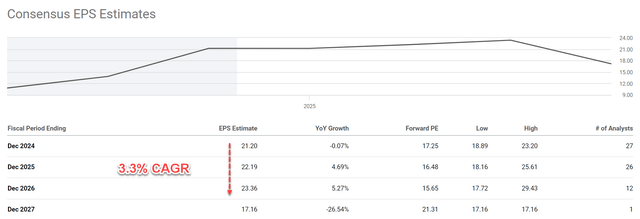

The chart beneath reveals how uninspiring Caterpillar’s (NYSE:CAT) earnings development is within the subsequent 3 years in line with analysts’ expectations. As seen, its EPS is projected to develop at a compound annual development fee (“CAGR”) of three.3% between FY 2024 and FY 2026. This interprets to an EPS of $21.2 in 2024 to 23.36 in 2026. Then in 2027, a large decline is anticipated to deliver its EPS again to $17.16.

Seeking Alpha

I could not utterly share the above consensus view (my development projections are detailed later). But I’m involved for a few causes. Besides the continuing geopolitical conflicts (wars are by no means good for infrastructure tasks), China’s softened demand is my most important concern.

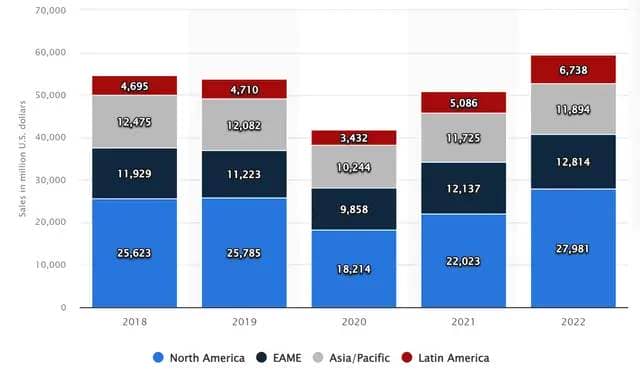

The chart beneath reveals Caterpillar’s international gross sales and income between FY 2018 and FY 2022 by area. As seen, CAT derives greater than half of its earnings from ex-U.S. markets. For instance, in 2022, solely about 47% of its income got here from the North American area. The Asia/Pacific area was the third-largest marketplace for Caterpillar as seen. CAT has reported that it expects its China gross sales to sluggish again in late 2022. In my view, the elements that brought about the slowdown again then have gotten worse now and might persist longer than anticipated. Our thought course of has been detailed earlier in one other associated article, and the gist is quoted beneath:

The actual property and infrastructure market in China stored struggling and its recent stimulus coverage appears to have restricted impact in my eyes thus far. We are nonetheless involved about China’s bother within the real-estate sector, a big shopper of uncooked supplies. We are seeing indicators that these troubles are removed from over, together with slumping new home gross sales, potential default dangers for heavy-weight builders, and hidden dangerous mortgage issues.

Statistica

Valuation threat is just too excessive

Despite the gloomy development outlook, the inventory trades at a excessive valuation. If you recall from the primary chart above, its ahead P/E ratio is estimated to be 17.25x based mostly on 2024 estimated EPS. This then would additional escalate to 21.3x in 2027 because of the earnings decline. To higher contextualize issues, CAT’s median P/E was round 16x solely prior to now decade. The valuation dangers could be seen from different metrics as properly. For instance, as proven within the prime panel of the subsequent chart beneath, CAT’s present price-to-CFO ratio is 14.57x. This can also be increased than its historic common of 12.13x by a large margin.

The most telling and excessive metric is its dividend yield in my opinion. As a dividend champion, it makes good sense to me to make use of its dividends as an approximation for its house owners’ earnings. As seen within the backside panel of the chart, CAT’s present dividend yield is 1.39%. It is barely about half of its historic common of two.66% and is on the lowest degree in a decade.

Seeking Alpha

Uninspiring return projections

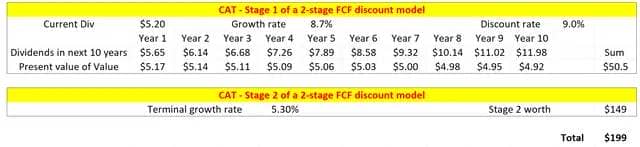

The mixture of low development and excessive valuation a number of has resulted in an unfavorable return profile in my opinion. As simply talked about, CAT is a dividend champion, with constant dividend will increase for greater than 25 years. Therefore, I feel it’s a good place to use the discounted dividend mannequin (“DDM”) to evaluate its return potential. To be on the extra beneficiant aspect, I’ll use a two-stage DDM mannequin, with the next development fee within the first stage to seize its previous development document and the second stage to seize its terminal development. As detailed in my earlier article:

There are a complete of three key parameters within the 2-stage DDM: the low cost fee, the expansion fee in stage 1, and the terminal development fee. For the low cost fee, I relied on the so-called WACC, the weighted common cost of the capital mannequin. The low cost fee for CAT is about 9% on common in recent years following this mannequin.

For the expansion fee within the 1st stage, I’ll extrapolate its dividend development prior to now (see the chart beneath once more as a result of I regard its dividend as a dependable indicator of its true house owners’ earnings).

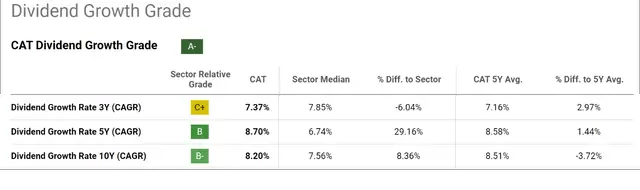

As seen, CAT’s dividend development has been round 8% prior to now 10 years. To wit, over the previous 3 years, the dividend development fee has been decrease at 7.37%. Looking additional again, the dividend development fee over the previous 5 and 10 years has been 8.70% and eight.20%, respectively. To be on the beneficiant aspect, I’ll assume it may proceed development at 8.7% for the subsequent 10 years.

Seeking Alpha

My technique for estimating the terminal development charges can also be detailed in my different articles. The outcomes are that:

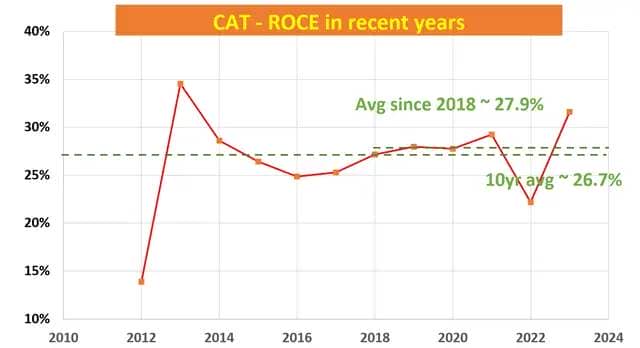

The technique includes the return on capital employed (“ROCE”) and the reinvestment fee (“RR”). The ROCE for CAT has been round 27.9% in recent years as seen within the chart beneath. Its RR is about 10% on common. With these inputs, CAT’s perpetual development fee could be ~2.8% (27.9% ROCE x 10% RR = 2.8%). Note this quantity is the actual development fee with out inflation. To receive a notional development fee, one would wish so as to add an inflation escalator. Assuming a median inflation of two.5% would deliver the terminal development fee to five.3%.

With all of the inputs prepared, the final desk on this part summarizes the outcomes from the 2-stage DDM. Here I used its FWD dividend of $5.2 per share. The backside line is that this mannequin reveals that the honest value of CAT is round $199. Compared to its present value of $365, I’m simply seeing an excessive amount of valuation threat right here.

Author

Author

Other dangers and last ideas

The article will not be balanced with out mentioning the upside dangers. The prime upside threat in my thoughts is the U.S. government-funded infrastructure investments. The authorities’s emphasis on updating the nation’s basic infrastructure may present a wholesome pipeline of tasks within the home market. However, it’s fairly unsure in my opinion and the U.S. market’s contribution to CAT’s income streams is proscribed. Another upside threat includes its Energy & Transportation phase. I count on this phase to be in fine condition, with stable general order ranges from the gasoline and energy era classes. Readers conversant in my writing know that I’m, typically, constructive in regards to the vitality sector beneath present circumstances. Finally, in the long run, the corporate is engaged on digital capabilities, autonomous methods, and the subsequent era of heavy tools, which could assist to gas development and enhance its margins.

All instructed, my general view is that CAT could current a very good case for short-term momentum merchants. It additionally makes a very good maintain case for current traders who’re really dedicated to the long run and watch for its fundamentals to meet up with valuation. As a possible investor, I feel the valuation dangers are too excessive beneath present circumstances.

{kind=link}