On the premise of insurance coverage firms’ bond investments, I look at how shifts in traders’ demand for company bonds have an effect on non-financial bond issuers. When demand for his or her bonds will increase, companies’ financing prices lower, which inspires them to extend their bond debt and make investments extra. These results crucially rely upon how credit-constrained companies are. My findings emphasise the important function that institutional traders play in shaping non-financial companies’ financing choices and actual financial exercise.

Corporate bonds and their traders

Corporate bonds function an important supply of financing for non-financial companies. In the United States, non-financial companies’ bond liabilities exceeded USD 6.7 trillion in 2022, which is greater than their mortgage liabilities.[2] While companies within the euro space are comparatively much less reliant on bond financing, its significance has additionally been rising in recent years (Berg et al., 2021; Darmouni and Papoutsi, 2022).[3]

This rising significance of bond financing locations bond traders within the highlight. How necessary are sure teams of traders for companies? Do they’ve any results on companies’ financing prices and choices? These questions are key for understanding the interplay between non-bank monetary intermediaries and the true economic system. In Kubitza (2023), I tackle these questions, utilizing information on insurance coverage firms domiciled within the United States.

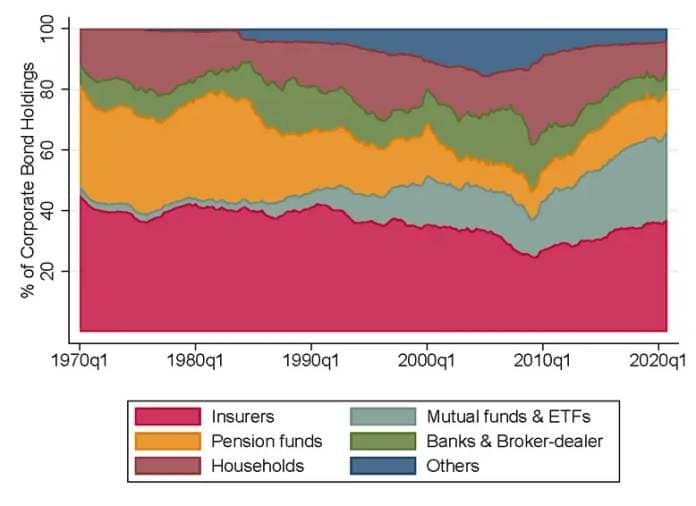

Corporate bonds are primarily held by institutional traders, equivalent to insurance coverage firms (Chart 1). Compared with (much less standardised) financial institution loans, bond possession is extra dispersed, and traders generally buy bonds within the secondary market (the place beforehand issued bonds are traded).[4] The conventional view has been that monetary markets are extremely elastic. This would imply that shifts in investor demand which can be unrelated to a agency’s fundamentals would haven’t any important impression on the agency’s financing prices and choices. Recent research problem this view, documenting that secure funding from bond traders can decrease a agency’s financing prices throughout occasions of monetary stress (Becker and Ivashina, 2014; Coppola, 2022). But how necessary are these traders in regular occasions, when monetary markets are comparatively liquid and companies face comparatively few monetary constraints?

Chart 1

Corporate bond holdings by investor kind

Source: Z.1 Financial Accounts of the United States, Release Table L.213.

Notes: This chart depicts the share of company bond holdings by investor kind within the United States after excluding international holdings. ETFs are exchange-traded funds. A broker-dealer trades in securities on behalf of its shoppers and in addition by itself behalf.

Insurance firms, premiums and bond investments

I take advantage of information on greater than 1,500 US insurance coverage firms to determine shifts of their bond demand. Insurers maintain practically 40% of US company bonds (Chart 1). Their main supply of financing is insurance coverage premiums from households, i.e. funds made by policyholders for cover in opposition to losses attributable to occasions equivalent to automotive accidents or windstorms. Higher premium revenue, for instance owing to elevated salience of dangers stemming from pure disasters, results in extra bond purchases by insurers within the secondary bond market. Given the magnitude of insurance coverage premiums – which amounted to roughly USD 1.7 trillion in 2019 within the United States – modifications in premium revenue correspond to important shifts in insurers’ demand for monetary investments, particularly company bonds.[5]

The set of companies that insurers spend money on (their “investment universe”) tends to stay nearly the identical over time. In reality, insurers are practically 14 occasions extra more likely to make new purchases of a agency’s bonds if they’ve invested in that agency beforehand. Building on this proof, I take advantage of the insurance coverage premiums collected by US insurers which have been previous bondholders of a agency to isolate shifts within the insurance coverage sector’s demand for that agency’s bonds.

It appears unlikely {that a} agency’s funding alternatives would correlate extra with households’ insurance coverage take-up when insurers have beforehand invested in that agency. Under this assumption, fluctuations in insurance coverage premiums – and ensuing bond purchases by insurers – can be unrelated to the funding alternatives of the companies that insurers spend money on. Several observations do in truth help this assumption. For instance, bond costs within the secondary market improve considerably following a rise in insurers’ bond purchases that’s pushed by insurance coverage premium progress (Chart 2). The worth dynamics rule out the likelihood that these outcomes mirror modifications in firm-driven bond provide (which would scale back costs) slightly than insurer-driven bond demand. As bond costs rise, companies’ financing prices within the main bond market (the place new bonds are issued) lower.

Chart 2

Secondary market bond costs and insurers’ bond demand

Notes: The chart depicts worth dynamics within the secondary marketplace for bonds of companies that see a rise in purchases of their bonds ensuing from premium revenue will increase in months 0, 1 and a pair of, relative to bonds of different companies. Specifically, it plots the estimated worth impression (dots) and its 90% confidence interval (bins) in foundation factors when insurers buy a further 1% of a agency’s excellent bonds within the quarter of months 0, 1 and a pair of. The estimates are primarily based on regressions of the cumulative return on bonds within the secondary bond market (computed relative to month -1) on insurers’ bond purchases as a share of the agency’s excellent bond debt, utilizing insurance coverage premiums as an instrumental variable.

Non-financial companies reply to modifications in traders’ bond demand

Firms are extremely conscious of constructive shifts in insurers’ funding demand. When, pushed by robust insurance coverage premium progress, insurers conduct extra purchases amounting to 1% of a agency’s excellent bonds, the agency’s bond debt grows by roughly 6 proportion factors (or 0.29 commonplace deviations) quicker. Thus, companies have a tendency to take advantage of beneficial financing circumstances to borrow extra within the company bond market.

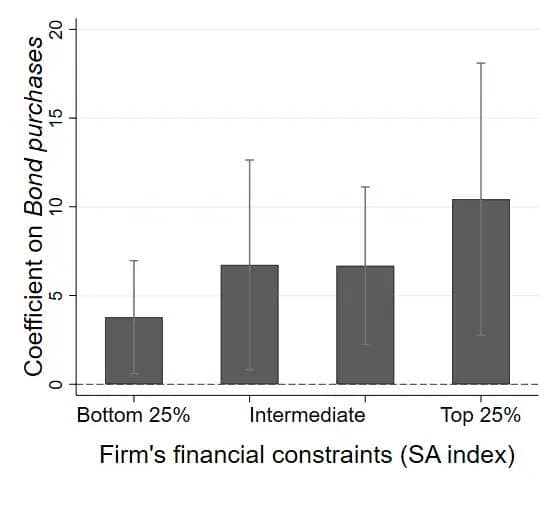

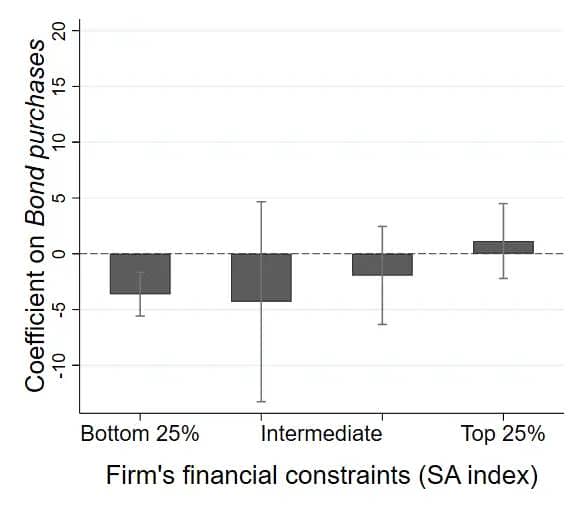

An necessary query is whether or not companies use the extra funding to switch different types of debt (e.g. financial institution loans) or to spice up funding. My outcomes present that companies’ monetary constraints have a major impact on their behaviour (Chart 3). Smaller and newer companies are usually extra financially constrained and, thus, are much less capable of seize worthwhile funding alternatives ex ante. I discover that these companies use the extra funding to considerably increase their funding actions, equivalent to acquisitions. By distinction, the least financially constrained companies use the extra funding to repay different debt that’s possible extra expensive than bonds or financial institution loans, equivalent to asset-backed securities.

Chart 3

Firms reply otherwise relying on their monetary constraints

|

When companies are extra financially constrained (greater size-age index), their complete funding responds extra strongly to investor demand for his or her bonds |

The least financially constrained companies scale back debt aside from bonds and loans in response to a rise in investor demand for his or her bonds |

|

(Dependent variable: complete funding) |

(Dependent variable: complete different debt) |

|

|

Notes: The chart depicts the response of a non-financial agency’s (a) complete funding and (b) complete “other debt” to the insurance coverage sector’s premium income-driven bond purchases. Specifically, it plots the estimated coefficients and 90% confidence intervals (proven by the whiskers) for bond purchases relative to excellent bonds (utilizing insurance coverage premium progress because the instrumental variable) individually for companies in numerous cross-sectional quartiles of the size-age (SA) index from Hadlock and Pierce (2010) in regressions with (a) complete funding and (b) complete “other debt” because the dependent variable. A bigger SA index signifies tighter monetary constraints. Total funding is the sum of acquisition expenditures and capital expenditures. Total “other debt” is complete debt excellent much less bonds, business paper, capital leases and financial institution loans.

Finally, whereas mildly constrained companies largely use the funding to extend their funding, in contrast to different companies they expertise a unfavorable inventory worth response. A attainable rationalization for this result’s that beneficial financing circumstances enable the managers of mildly constrained companies to pursue much less worthwhile funding initiatives, e.g., “pet projects”, that shareholders would possibly object to – i.e., free money circulation issues (Jensen, 1986).

In abstract, the outcomes counsel that the implications of shifts in bond demand differ significantly throughout companies. On the one hand, will increase in bond demand can ease financing frictions for very constrained companies. On the opposite hand, they could additionally exacerbate free money circulation issues for mildly constrained companies.

Conclusions

As non-financial companies have gotten more and more reliant on bond financing, it’s crucial to know the function of bond traders in company choices and financial exercise. This analysis reveals that traders, by their impression on bond costs, can have a major affect on the financing and funding choices of non-financial companies.

Thus, whereas the transition from bank-based to market-based economies could diminish the affect of banks on companies, it possible amplifies the significance of investor demand. The scale and effectivity of traders’ affect hinges to an incredible extent on their impression on costs in monetary markets, in addition to the character and depth of the financing constraints that non-financial bond issuers are topic to.

Because bond issuers are usually much less credit score constrained than bank-reliant companies (Cantillo and Wright, 2000), a bigger funding response could be anticipated to mortgage provide shocks than to bond investor demand shocks. However, combination results of investor demand additionally rely upon bond market liquidity, the share of companies with bond market access and the impression of bond investor demand on companies’ propensity to enter the bond market. In economies with a rising bond market, such because the euro space (Darmouni and Papoutsi, 2022), traders could have a very robust impression on bond costs and companies could also be desperate to broaden their bond financing, suggesting that investor demand could also be extremely necessary despite the fact that a big share of companies at the moment depend on financial institution financing.

References

Becker, B. and Ivashina, V. (2014), “Cyclicality of credit supply: Firm level evidence”, Journal of Monetary Economics, Vol. 62, pp. 76-93.

Berg, T., Saunders, A. and Steffen, S. (2021), “Trends in corporate borrowing”, Annual Review of Financial Economics, Vol. 13, pp. 321–340.

Bolton, P. and Scharfstein, D. S. (1996), “Optimal debt structure and the number of creditors”, Journal of Political Economy, Vol. 104, pp. 1-25.

Cantillo, M. and Wright, J. (2000), “How do firms choose their lenders? An empirical investigation”, Review of Financial Studies, Vol. 13, pp. 155-189.

Coppola, A. (2022), “In safe hands: The financial and real impact of investor composition over the credit cycle”, Working Paper.

Darmouni, O. and Papoutsi, M. (2022), “Europe’s growing league of small corporate bond issuers: New players, different game dynamics”, VoxEU Column, 8 July 2022.

Hadlock, C. J. and Pierce, J. R. (2010), “New evidence on measuring financial constraints: moving beyond the KZ index”, Review of Financial Studies, Vol. 23, pp. 1909-1940.

Jensen, M. C. (1986), “Agency costs of free cash flow, corporate finance, and takeovers”, American Economic Review, Vol. 76, pp. 323-329.

Kubitza, C. (2023), “Investor-driven corporate finance: evidence from insurance markets”, Working Paper Series, No 2816, ECB, May.

{kind=link}