Rates on 30-year fixed-rate mortgages averaged 6.74% the week of March 14, 2023, in line with Freddie Mac. The mark represents a 1.29% drop from the speed’s 23-year excessive of 8.03% in October 2023. And whereas charges have cooled since that October peak, they continue to be elevated. Consequently, the cost of borrowing is increased than in recent years, making it dearer for homebuyers to buy houses and for current owners to refinance their mortgages.

But excellent news may very well be on the horizon. The Federal Reserve has signaled it can lower its goal charge 3 times in 2024. Experian seems to be nearer at what that might imply for mortgage charges.

How do rates of interest have an effect on mortgage prices?

Mortgage rates of interest have a direct impression on housing affordability. Not solely do charges issue into the general cost of a home mortgage, however decrease charges additionally imply decrease month-to-month funds (and vice versa).

Rate adjustments don’t have any bearing on current fixed-rate mortgages, which have the identical rate of interest and month-to-month fee for the whole lot of the mortgage’s time period. However, mortgage charges do impression the general cost and month-to-month fee quantity of latest fixed-rate mortgages and refinance loans. Adjustable-rate mortgages (ARMs) are additionally impacted by charge adjustments all through the mortgage’s time period.

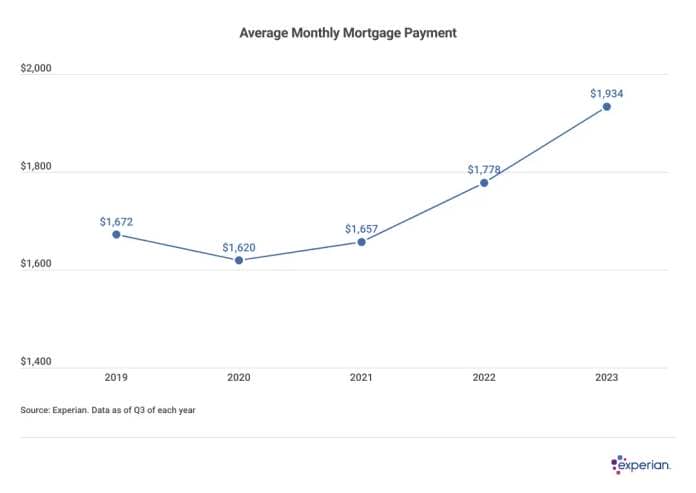

To illustrate, in September 2020, when common charges have been right down to 2.90%, the common month-to-month mortgage fee was $1,620, in line with Experian knowledge. Rates went on to hit a report low in January 2021, then started to climb in 2022. By September 2023, when common mortgage rates of interest climbed to 7.31%, mortgage funds have been a mean of $1,934 a month.

Is the federal reserve anticipated to chop charges in 2024?

At its December assembly, the Fed signaled it will lower the federal funds rate 3 times in 2024—leading to a 0.75% charge lower by 12 months’s finish. Most economists anticipate any charge cuts will not occur till the second quarter, on the earliest.

If the Fed follows by means of on charge cuts, it will mark a stark reversal from an aggressive cycle of charge hikes because the Fed sought to curb inflation. Beginning in March 2022, the Fed elevated the federal funds charge 11 consecutive occasions—essentially the most aggressive collection of will increase in 4 many years. The benchmark charge has remained within the 5.25% to five.50% vary for the reason that most recent hike in July 2023.

If and when mortgage charges drop, debtors will profit from decrease borrowing prices and month-to-month funds. For instance, if mortgage charges drop 0.75%—in step with the projected federal funds charge lower—you possibly can save $750 in curiosity yearly for each $100,000 you borrow, or $22,500 in curiosity costs over a 30-year time period.

How federal reserve charge cuts have an effect on mortgages

Banks sometimes set their prime charge by including 3% to the federal funds charge. As of March 2024, the federal funds goal vary was 5.25% to five.50% and, accordingly, the prime charge was 8.50%. Keep in thoughts, the Federal Reserve would not set mortgage charges, however its actions do affect them. For instance, mortgage charges climbed considerably in the course of the Fed’s charge hikes in 2022 and 2023.

Rate cuts might make mortgages extra reasonably priced

If the Federal Reserve lowers the federal funds charge, mortgage charges might observe swimsuit. We’ve already begun to see proof of this development, with lenders adjusting charges in anticipation of the anticipated Fed actions. In December 2023, when the Fed first projected charge cuts in 2024, mortgage charges declined sharply, partly on account of projected cuts.

Mortgage charges modify every day in response to the dynamics of the U.S. and world economies. When the Fed in the end decides to cut back the federal funds charge, the market might reply by reducing charges even additional.

Lower mortgage rates could be welcome information for brand spanking new homebuyers who’ve been sidelined by excessive mortgage rates of interest. And owners with ARMs or home equity lines of credit (HELOCs) might see their charges and month-to-month funds drop.

Mortgage approval might get simpler

Because decreased mortgage charges would end in decrease month-to-month funds, debtors might discover it simpler to qualify for a brand new home mortgage. That’s as a result of a decrease fee decreases your debt-to-income ratio (DTI), a significant component home lenders contemplate when qualifying you for a brand new mortgage. Your DTI is the share of your month-to-month debt obligations in comparison with your gross month-to-month revenue. Lenders often don’t desire your complete month-to-month debt funds to exceed 36% of your month-to-month revenue, with 28% allotted on your housing fee.

Is It higher to purchase now or look forward to charges to fall?

Buying a home now is a viable possibility if you happen to can comfortably afford the month-to-month mortgage fee, upkeep prices and taxes at at the moment’s rates of interest. After all, you possibly can all the time refinance later to snag a decrease mortgage charge and fee.

Additionally, if mortgage charges proceed to fall, home costs might rise. Remember, many individuals have been unable to afford a home on account of excessive rates of interest. If charges drop, extra homebuyers might buy houses, and the elevated demand might drive up home costs.

On the opposite hand, a charge decline might deliver extra houses to the market, easing competitors. According to Zillow, 80% of current mortgages have rates of interest under 5%. That’s as a result of owners locked in these traditionally low charges in 2021 earlier than charges escalated. If charges fall, extra owners could also be prepared to promote if they will safe decrease rates of interest on their subsequent home. More home listings might ease the present provide scarcity and assist curb rising costs.

Trying to time the market may very well be a feeble train for the reason that housing market and the Fed’s coverage strikes are sometimes unpredictable. As such, contemplate the affordability of any home buy and your willingness to refinance later for a decrease charge as major elements in your choice.

If you determine to tug the set off on a brand new home, contemplate the next tips to make your home buy extra reasonably priced.

-

Take steps to improve your credit. Lenders have a tendency to increase their greatest charges to debtors with higher credit score. Reduce bank card balances, deliver any late funds present and pay all of your money owed on time going ahead to begin bettering your credit score scores.

-

Save for a down fee. The bigger your down fee, the decrease your loan-to-value (LTV) ratio—the quantity of money it is advisable borrow versus the home’s present market worth. Lenders sometimes view debtors with decrease LTVs as much less dangerous, which might end in a decrease rate of interest. You might additionally get rid of private mortgage insurance on a traditional mortgage with a 20% down fee. PMI is often added to your month-to-month mortgage fee and sometimes equals 0.5% to 2% of your complete mortgage quantity.

-

Lower your DTI. Lenders take an in depth take a look at your DTI to gauge your potential to afford a brand new mortgage mortgage. Most lenders require DTI ratios under 36%, however some might permit as much as 45%. Some Federal Housing Administration-backed home loans permit DTIs as much as 50% when you have giant money reserves.

-

Opt for a shorter mortgage time period. The 30-year fixed-rate mortgage is the preferred kind of mortgage however often options increased rates of interest than shorter loan terms for 15 or 20 years. If you possibly can afford the upper funds of a shorter-term mortgage, it’s possible you’ll save considerably on curiosity costs over the lifetime of your mortgage.

Make positive your credit score and funds are in good condition

If you are contemplating shopping for a home, be certain your monetary state of affairs and credit score are squared away to make the most of probably decrease mortgage charges. If attainable, pay down money owed to decrease your DTI ratio and save for a bigger down fee. Shore up your credit score by reviewing your credit score report and credit score rating. Address any points you discover and take proactive steps to improve your credit fast.

This story was produced by Experian and reviewed and distributed by Stacker Media.

{kind=link}