It seems excessive LVR lending is not to debtors making an attempt to get on to the property ladder; reasonably it’s being utilized by debtors who’re eager to stretch themselves into properties they could not in any other case afford.

That is one interpretation from the RBNZ March knowledge launched this week in each their C31 and C33 collection.

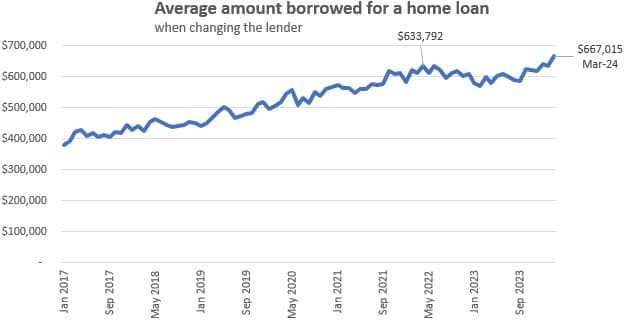

And home mortgage debtors who change lenders are borrowing a document $667,000 on common. That new document got here in March 2024.

But those self same debtors who borrow on a excessive LVR foundation are committing to $700,000 on common.

High LVR debtors are, it appears, not afraid to commit. You may need thought that top LVR lending was for low-income debtors eager to get on to the property ladder in modest purchases suited to their stage in life. But reasonably it appears to be for individuals who select to stretch.

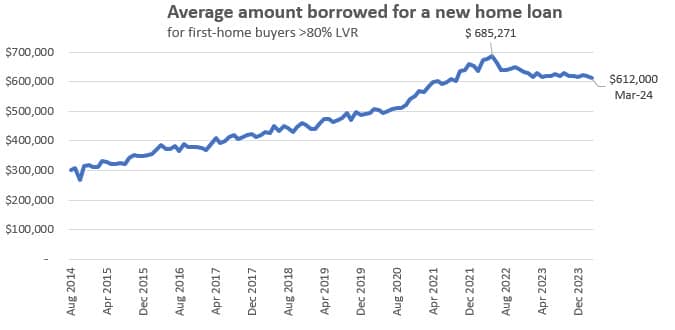

First home patrons commit on common to $548,000, however high-LVR FHBs decide to $612,000. These are the borrowed quantities. But how a lot are they paying for the home? you could find that estimate right here.

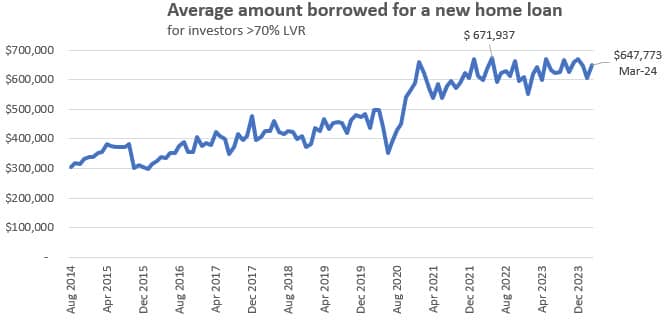

And the high-LVR story extends to traders too. On common residential property traders borrow $515,000 whereas excessive LVR debtors are stretching to +25% extra at almost $648,000.

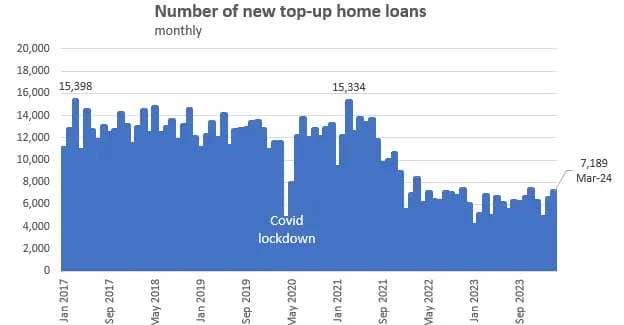

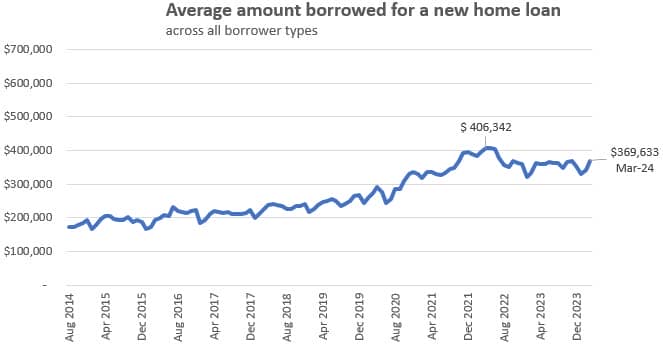

Over all home loans, the typical home mortgage measurement in March 2024 was slightly below $370,00, and a key purpose that common appears low is due to top-up loans.

The common top-up quantity borrowed was $103,000 in March 2024, and that’s down -17% from the early 2022 peak. There have been 7189 top-up loans made in March 2024. But that was down an enormous -53% from the 15,300 stage in March 2021.

The story is analogous for many forms of home mortgage – the March 2024 volumes are far lower than their peak ranges.

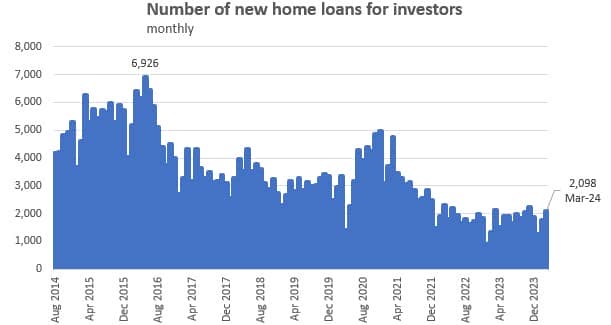

Overall, loans to traders fell a startling -70% from 6926 in March 2016 to solely 2098 in March 2024.

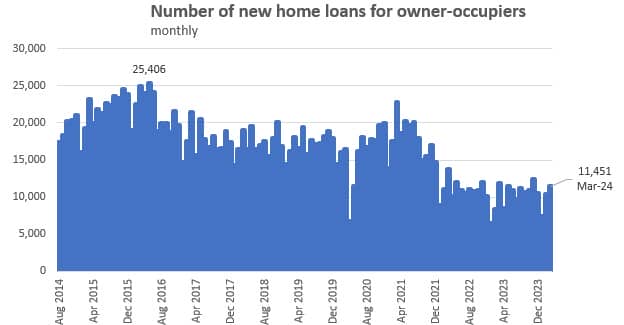

Loans to owner-occupiers are -55% decrease from their March 2016 stage of 25,406, now solely 11,451 in March 2024.

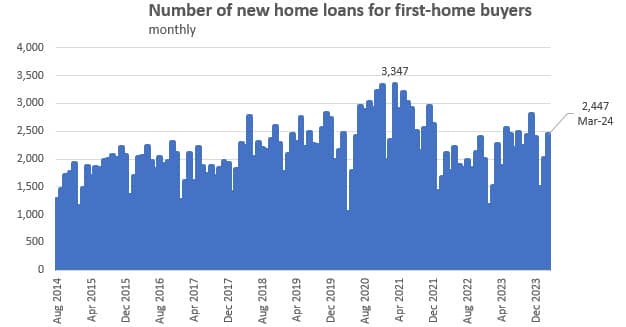

So that makes the -27% fall in FHB loans the least-affected sector and it raises the relative stage of FHB exercise general in a shrinking-volume market.

Falling home mortgage volumes and easing home mortgage values paint an image of a mortgage market that has fallen right into a funk. None of those charts describe the rollover / refinancing market which is the most important a part of the financial institution home mortgage business, however they do shine a highlight on a sector that’s in its quietest interval over the previous decade.

Real property brokers may be capable of survive this quietish interval by promoting fewer increased priced houses, conserving the “median costs” reported at related ranges, and mortgage brokers can survive as the majority of the refinance/rollover market churns. But it’s clear this isn’t at present a rising marketplace for both. Market share issues extra to everybody, together with the banks, when they’re all in a no- or low-growth sector.

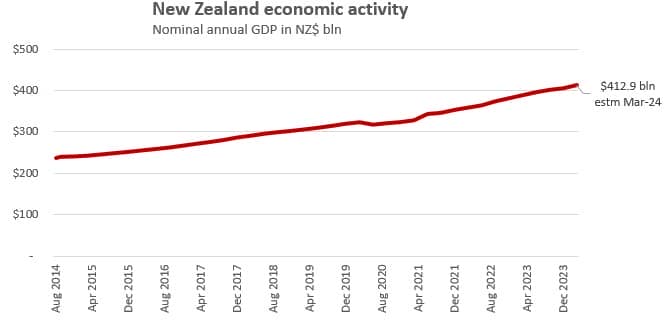

In distinction, general financial exercise has not missed a beat but, nonetheless increasing in nominal phrases (and the nominal world is the place the true property and mortgage market lives). So maybe we’re pushing the extreme fascination with ‘property’ down in our collective relative priorities.

{kind=link}