2023 is poised to be a document 12 months for cat bond issuance and a key issue is the UK’s transient monetary disaster final 12 months, which reminded pension fund managers across the globe of the significance of liquidity, in keeping with Leadenhall Capital Partners CEO Luca Albertini.

Speaking at The Insurer’s Pre-Monte Carlo Forum, Albertini stated: “Brokers have indicated that in the first half of this year, there were as many cat bond issuances as last year, showing that investor demand has been very healthy.”

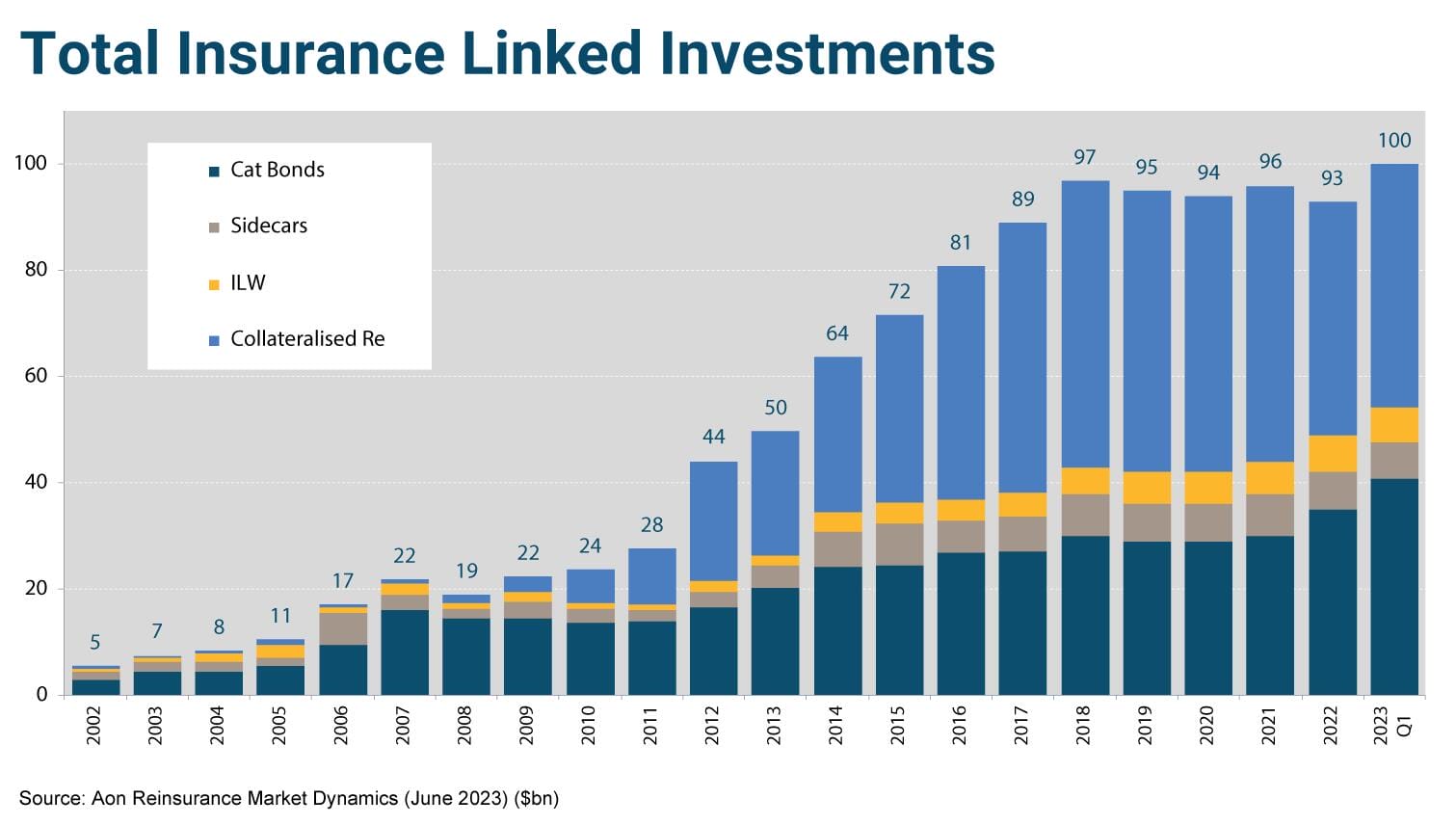

But he contrasted this with collateralised reinsurance placements, the place pension funds – the biggest part of the ~$100bn ILS market – stay cautious on points resembling trapped capital and restricted liquidity.

Albertini additionally referenced the robust “double-digit” returns which can be presently accessible to cat bond traders. At H1 2023, the Swiss Re cat bond index – which measures complete returns on excellent cat bonds – was up 10.3 p.c. Indeed, after a robust July-August, it’s wanting more and more seemingly that the authoritative index’s document annual return of 15 p.c in 2007 could also be exceeded this 12 months.

In addition to robust returns, nevertheless, pension funds are notably involved about liquidity after UK life insurers in September and October 2022 had been confronted with margin calls after leveraging their gilt portfolios with liability-driven investments. It sparked a mini confidence disaster till the Bank of England stepped in to stabilise the markets, a key issue within the exit of British Prime Minister Liz Truss.

While sidecars, trade loss warranties and collateralised XoL reinsurance placements are locked in, the secondary marketplace for cat bonds gives traders with the extra reassurance of liquidity within the occasion an early exit is required, Albertini defined.

“Clearly, there has been a shift to liquid strategies,” he stated.

“Yes, you still have the risk of collateral trapping but you can trade out within two weeks [with cat bonds].”

On the difficulty of trapped collateral, Albertini estimates that round $20bn – or “20 percent give or take” – of the $100bn ILS market is presently locked. This means it would both be returned to traders or drawn right down to cowl incurred losses, however within the meantime can’t be deployed as dwell threat capital.

Speaking to an viewers of almost 300 London executives, he stated ILS fund managers like Leadenhall Capital stay involved about extreme trapping of capital.

“Of course, collateral trapping is a prudent way to manage the development of reserves, especially when there is uncertainty, but it is very hard to find clarity and to properly codify,” he famous. Albertini added that he’s at instances sceptical when loss estimate reserves are steadily set near positions that allow a dealer to lock increased layer positions.

He reminded the viewers that it’s a tough market with capability much less freely accessible and fund managers could merely determine to not renew if the behaviour is “abusive”.

“So a few of the behaviour when it is abusive will likely be punished by having much less capital accessible. It is a part of being moral and being and being smart in creating relationships.

“I’m Italian, I remember and I keep a grudge,” he joked to the viewers.

ESG

The Leadenhall Capital founding associate concluded with warnings that capital administration companies will more and more contemplate the ESG credentials of reinsurance corporations within the face of mounting regulatory obligations.

“On ESG, we’ve heard a lot about net-zero initiatives in the reinsurance space. For us, this is becoming very topical,” he stated.

“This is currently being embedded in European litigation, firms will have to declare where they stand. It’s increasingly risky from an investment management standpoint to say you don’t consider ESG – but if you do declare and then don’t follow through, you may be fined for greenwashing.”

For Leadenhall Capital, Albertini stated which means at issuance, all positions will likely be rated on a three-tier site visitors gentle system utilizing each qualitative and quantitative features, together with ESG elements.

As local weather change stays a major reservation for traders when it comes to forward-looking modelling horizons, the agency may also perform an evaluation of a reinsurer’s environmental credentials, together with plans on find out how to navigate the reinsurance e-book by means of the net-zero transition, in addition to the funding e-book.

And on governance, whereas holding totally different meanings relying on the corporate, for reinsurers that is usually translated in underwriting efficiency and reserving coverage.

“For me, it’s about transparency in reserving, how robust is your underwriting, and the pipeline in delivering value for shareholders and securing capital,” Albertini concluded.

{kind=link}