*Coal stocks at energies, CIL mines up 30% y-o-y

*Lower-than-expected thermal generation reduces stock circumstance

*CIL’s dispatches to non-power sector increases 45% in Apr’23

India is making progressive efforts to equal skyrocketing power need which is putting a high level of pressure on the coal-fired energies that represent around 70% of domestic energy generation.

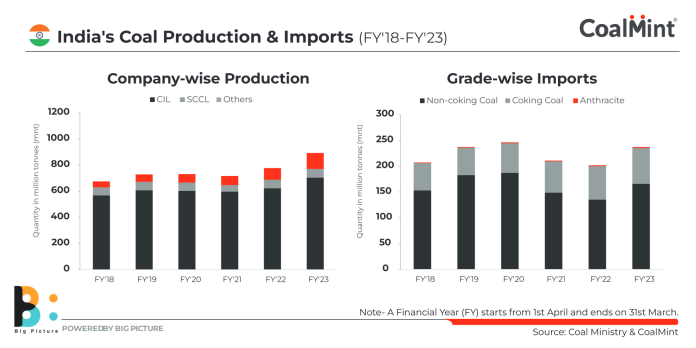

The nation tape-recorded historical development in its coal output at 892.21 million tonne (mnt) in FY23. Total production was 15% greater compared to 777 mnt in FY22. Despite this, India’s coal imports increased greatly by around 18% y-o-y to over 237 mnt in FY23 from 202 mnt in FY22, CoalMint information programs.

Out of overall import deliveries, those of non-coking or thermal coal stood at over 166 mnt, which is approximately 70% of overall imports. Non-coking coal imports edged up by 23% y-o-y on greater need from power manufacturers and with the federal government mandating imports to satisfy peak power need.

Imports increased likewise due to shortage developing from logistical traffic jams and the dominating policy of supply prioritisation for the power sector by state-owned miner CIL, which is requiring the non-power sector to choose imports.

Coal stock circumstance

Total coal stock available at power plants and mines run by CIL is examined at 100.45 mnt at the end of April, up 28% from year-ago levels.

This shows large enhancement from the duration when stock had actually plunged arising from greater coal intake throughout summer season and lower materials in monsoon.

Nonetheless, offered the considerable bearing of the power sector on the supply chain and the consistent disturbance which has actually ended up being a cyclic phenomenon, imports are inevitable.

Unseasonal rains

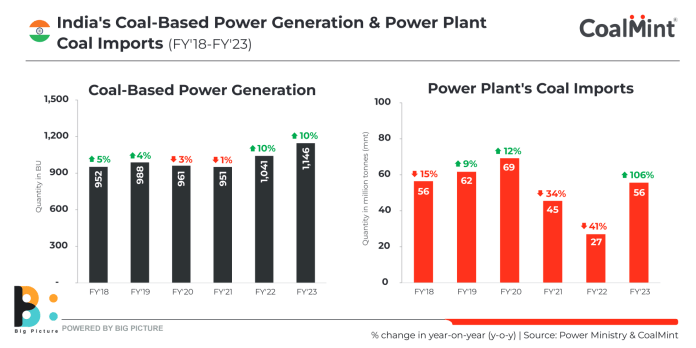

Coal-based power generation grew partially by 0.2% y-o-y to 105.9 billion systems (BU) in April as versus 105.64 BU in April 2022.

The can be credited to the unseasonal rains in lots of parts of the nation which minimized need for electrical power in the continuous summer season duration. So coal intake was not as strong as was forecasted previously.

However, generation volume increased by 6% m-o-m to 3.53 BU/day in April as versus 3.33 BU/day in March, to make up for the generation loss from alternate source of power, for example the little generation of hydropower throughout the summer season with a drought-like circumstance dominating in various areas of India.

So, stock levels at power stations dropped in April following a constant build-up tape-recorded over the previous 6 months. The m-o-m stock liquidation compared to March was 1.1 mnt as versus 3.5 mnt in the year-ago duration.

To guarantee sufficient power accessibility, the Ministry of Power (MoP) has actually advised power plants to import 6% (by weight) of their coal requires for mixing functions till September this year. A comparable required had actually been released in 2015 too. That time, the mixing ratio was kept at 10%.

As per federal government required, NTPC, India’s biggest power manufacturer, has actually chosen to import around 5.4 mnt of coal throughout the very first half of FY24 however no tender has actually been drifted recently.

Dispatches to non-power sector

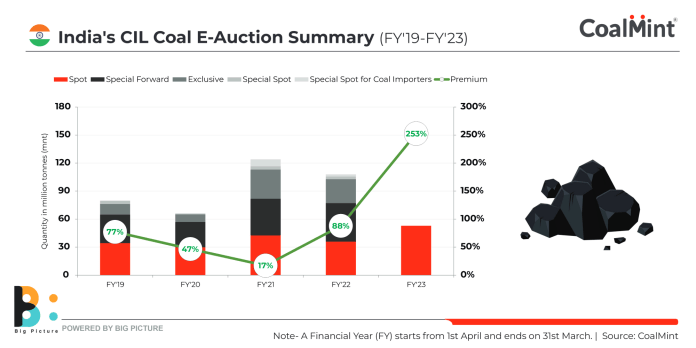

CIL stepped up supply policy to guarantee greater volumes for the power sector which led to minimized amounts being used in e-auctions. Notably, overall sales by means of auctions dropped to the most affordable level in the previous 7 fiscals in FY23.

However, progressive build-up of stock at mines and controlled coal-fired power generation suggest there is increasing probability that CIL will designate more volumes for sale by means of auctions this year.

Early indications have actually been motivating in regards to supply enhancement for the non-power sector. CIL’s dispatches to the end-user market signed up 44% development to 11.8 mnt throughout April, which is the greatest ever tape-recorded in April up until now.

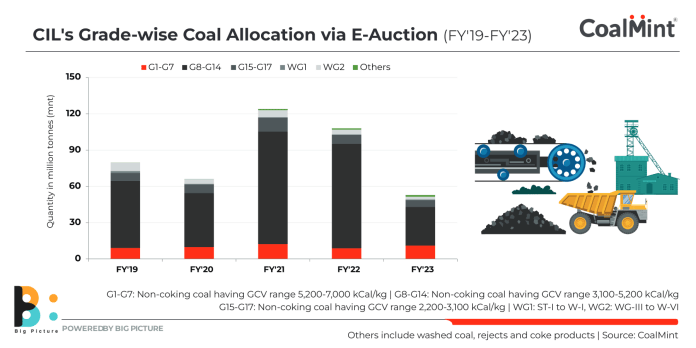

A grade-wise split of auction sales reveals that allowance in the high-CV basket increased in spite of general volumes falling in 2015. With CIL subsidiaries preparing to even more scale up production, there are possibilities of improved accessibility of quality product especially from Eastern Coalfields (ECL) and North Eastern Coalfields (NECL).

Another crucial reason auction sales might increase in the near-term is correction in domestic coal rates on international market hints.

Outlook

In view of the steady stock circumstance and company procedures already in location to reinforce domestic materials, it is not likely that imports by the energies will increase in the coming quarter unlike in 2015.

However, there are projections of heatwaves in lots of parts of the nation and pre-monsoon restocking activity will sustain interest in imports.

The federal government is likewise dealing with a ‘monsoon management strategy’ to guarantee sufficient accessibility of fuel at power plants throughout the rainy season when both coal production and evacuation are affected. So, if any abrupt increase in power need is dealt with effectively it will cause much better circulation of coal throughout sectors.

Global cost characteristics likewise impact imports. For example, a cement significant has actually minimized thermal coal imports this year in favour of family pet coke of United States origin due to international cost correction of the latter product. Moreover, international products require effect the efficiency and basic material sourcing of commercial users such as aluminium manufacturers.

In order to enhance domestic coal accessibility, the federal government has actually set a target to produce 1,012 mnt of coal in FY24. The production target for CIL has actually been repaired at 780 mnt, Singareni Collieries (SCCL) at 70 mnt, while the staying output of 162 mnt is anticipated to come from a variety of slave and business miners.