NEW YORK CITY (ICIS)–With the last wave of brand-new

capability additions and relieving of logistics

restraints, the United States petrochemical sector has actually a

clear course to improving exports to brand-new records

in 2023, heading into this year’s International

Petrochemical Conference (IPC).

Even with a recessionary worldwide financial

outlook moistening need overseas and capability

rising in China, the United States cost benefit is

merely undue to keep back the floodgates.

The United States exported a record 11m tonnes of

polyethylene (PE) in 2022 as production from

brand-new crackers and acquired plants sped up

– up 25% from 2021 and exceeding the previous

record in 2020, according to the ICIS Supply

and Demand Database.

In chemicals and plastics, PE is the top

United States export without a doubt, and volumes ought to rise even

greater in 2023 as Shell’s Pennsylvania cracker

and downstream PE capability increases and as

Bayport Polymers’ (Borealis/TotalEnergies) PE

job in Texas comes online in Q2 2023.

In Canada, NOVA Chemicals’ direct low density

polyethylene (LLDPE) job is likewise anticipated

to start up in H2 2023.

United States PE exports in January 2023 consisted of 42.2%

of overall sales after reaching a record high of

46.7% in December and balancing 38.5% for all

of 2022, according to information from the American

Chemistry Council (ACC) and Vault Consulting.

“I think PE exports that balanced 39% of

overall sales in 2022 will leap up to 43-46% of

overall sales this year, which would be a brand-new

record in regards to volumes for the market,”

said Brian Pruett, senior vice president, PE at

Chemical Data (CDI), part of ICIS.

This will be driven by the 2nd wave of brand-new

United States and Canada PE capability of around 9bn lb/year

(4.1m tonnes/year) from Q4 2021 to Q3 2023

requiring to discover a home, weak domestic need in

H1, low natural gas-based feedstock expenses that

permit manufacturers to improve exports into greater

oil-based feedstock areas, extra

storage facility capability and the easing of logistics

restraints that had actually held PE exports back, he

included.

LOGISTICS RESTRAINTS

RELIEVE

The US need to export around 45% of its overall PE

production to keep operating rates at 90%

following the latest wave of capability

growths.

PE exports were constrained for much of 2022 by

logistics obstacles that led to regular

delivery hold-ups originating from lacks of

truck drivers, storage facility space and container

ship schedule.

As need for container ships declined in H2

2022, these logistics problems have actually likewise faded,

leading to exports as a portion of overall

sales breaching the 40% limit in August and

staying above that level for the rest of

the year.

It is not simply United States PE exports that are rising.

United States ethylene glycol (EG) exports soared 33% in

2022 from 2021, while United States polyvinyl chloride

(PVC) exports increased 26% year on year, according

to the ICIS Supply and Demand Database.

Increased United States EG exports are anticipated to

help plug

the supply gap in northeast Asia

throughout a heavy turn-around season in Q2.

EG purchasers in northeast Asia anticipate the

scheduled capability loss in the area to be

alleviated by an increased inflow of United States freights.

Over 75,000 tonnes have actually been repaired for shipment

into China in between the 2nd half of April and

early June.

On the PVC side, United States exports may

have plateaued for

the minute at reasonably high levels as costs

have actually increased and China’s market has actually been sluggish

to awaken. Exports from China’s oversupplied

market continue to stream into worldwide markets.

United States petrochemical exports will encounter a huge

headwind from a rise of brand-new jobs beginning

up in China. China will be including record-breaking chemical

and fertilizer capability in 2023 of almost 140m

tonnes/year, overshadowing the previous record of

over 90m tonnes/year in 2014 and driving worldwide

oversupply, according to an ICIS analysis.

China is the biggest importer of PE without a doubt, however

accounted for less than 11% of US PE exports in

2022, with the wider northeast Asia region

accounting for around 14%, according to the

ICIS Supply and Demand Database.

US polymers exports to Brazil will also face a

new headwind in the form of higher import

duties announced in March.

This will bring tariffs up for ethylene and

propylene copolymers, PVC and polyethylene

terephthalate (PET) to 11.2% from previous

levels ranging from 3.3-4.4%.

TREMENDOUS COST

ADVANTAGE

Buoyed by low-cost and abundant supplies of

natural gas liquids (NGLs), US ethylene and

derivatives producers continue to experience a

tremendous cost advantage from a global

standpoint, enabling greater volumes of

exports.

For LLDPE – the leading grade for US PE exports

– US spot margins from ethane feedstock were

close to $800/tonne as of late March. This

compares to margins in the $100/tonne range in

northeast Asia and the $200/tonne range in

northwest Europe on a spot basis – both based

on naphtha feedstock, according to ICIS Margin

Analytics.

CDI forecasts US natural gas prices averaging

close to $3/MMBtu in 2023 versus around

$6/MMBtu in 2022 with prices gradually moving

from the low $2/MMBtu level to the high

$3/MMBtu range by the end of 2023.

“In response to the collapse in prices over the

past month, producers have responded by cutting

production, or slowing down completion rates

for bringing new wells online. The market

response to a price signal is up to six

months,” said Barin Wise, vice president –

feedstocks and fuels at CDI.

On the demand side, the Freeport LNG export

terminal which had been offline since a fire in

June 2022 should be fully operational by early

April. Low prices also ushered in some

coal-to-gas fuel switching. This has moderately

increased demand from utilities which is not

expected to reverse over the next few months,

he added.

“Easing production rates and greater demand

tightens the balance, which leads to the

forecasted price gains later this year and in

2024,” said Wise.

Yet the US petrochemical feedstock cost

advantage based on natural gas should remain

firmly intact, as long as crude oil prices

linger at relatively high levels. As a rule of

thumb, US producers maintain an advantage as

long as the oil/gas price ratio ($/bbl

Brent/$MMBtu) is higher than 7x, according to

Kevin Swift, ICIS senior economist for global

chemicals.

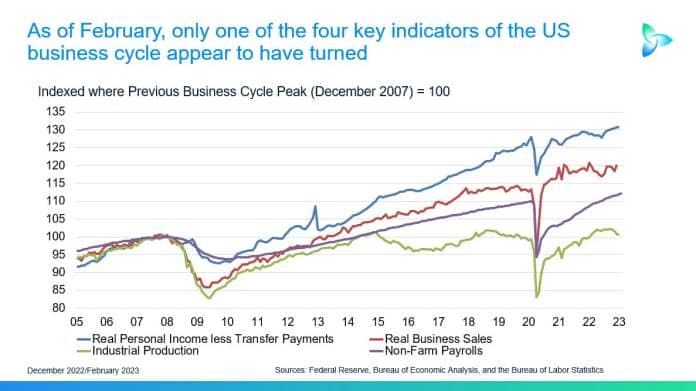

DEMAND AND DESTOCKING

On the US demand side, the near-term economic

outlook is no doubt challenging with the ISM US

Manufacturing Purchasing Managers’ Index (PMI)

in contraction territory (under 50) for the

fourth consecutive month in February.

Weakening demand in H2 2022 led to severe

inventory destocking across chemical chains,

which continues into Q1 2023. This is

particularly being felt in housing and

construction end markets, as well as markets

closer to the consumer such as do-it-yourself

(DIY) architectural coatings, electronics,

appliances, kitchen and bakeware, and even

personal care.

For the key US PE market, destocking largely

continues but should come to an end by Q2.

“After pulling 1.2bn lb (544,000 tonnes) out of

inventory in the last five months of 2022,

there was a 270m lb build in January that puts

producers at four days of supply above normal,”

said CDI’s Pruett.

“Downstream from producers, 80% of buyers are

still destocking, which should continue for

another 1-2 months,” he added.

Even when the PE destocking cycle ends, there

is unlikely to be a V-shaped recovery as

overcapacity will linger amid sluggish economic

conditions.

“With more PE capacity in the second wave

starting up in H1 2023 and ramping up to full

rates by Q3, oversupply should last until Q4,

but it will also depend on how hard or soft a

recession the US has, and when it begins,” said

Pruett.

Dow CEO Jim Fitterling in mid-March said the

new PE capacity coming on will “take about a

year to absorb”.

“You’ve got new supply coming on in the near

term, some lower demand from destocking [and]

some from durable goods reductions, and so

that’s put pressure there. While integrated

margins are improving through the quarter,

they’re certainly a long way from where they

were in Q1 last year,” said Fitterling at the

JPMorgan Industrials Conference.

US REGIONAL BANKING CRISIS AND ECONOMIC

OUTLOOK

For the US economic

outlook, inflation has been the number one

concern. But the US Federal Reserve’s series of

aggressive interest rate hikes to tame such

inflation is now putting major stress on the

country’s regional banking system.

The failure of two sizeable banks (Silicon

Valley Bank, Signature Bank) in the US and the

crisis of confidence contagion spreading to

other regional banks and European financial

institutions threatens to significantly tighten

lending conditions at the very least, further

slowing economic growth and potentially tipping

US and European economies into recession.

The implications for the economically sensitive

chemical industry are huge, as a major step

down in GDP growth or a contraction would

crater demand in an already weak environment.

The US regional banking crisis reduces the odds

of a soft landing, and the ICIS base case is

still a mild recession lasting 2 to 3 quarters.

Stabilising the financial system will be

critical to keeping it mild.

ICIS projects US GDP growth will slow

dramatically from 2.1% in 2022, to just 0.6% in

2023 with global GDP growth shrinking from 2.8%

in 2022, to 1.8% in 2023.

US housing starts, highly sensitive to interest

rates, are expected to plunge 19% to 1.26m in

2023. US light vehicle sales are projected to

rebound 7% to 14.7m units in 2023 on easing

supply chain constraints, but remain well below

the pre-pandemic 2019 level of 17.0m.

“I still believe a recession is inevitable.

That would be my base case,” said ICIS senior

economist Swift, pointing to leading

indicators, the severely inverted yield curve,

Fed tightening, declining monetary growth, the

ISM Manufacturing PMI and the downturn in

housing.

CHANGES IN BEHAVIOUR FROM COVID-19,

GEOPOLITICAL TURMOIL

The trauma on supply chains from the pandemic

and geopolitical turmoil is fostering

reshoring, which is supporting business

investment at a time when interest rates are

rising and margins are being squeezed.

“Normally higher interest rates or moderated

cash flow would work to pause investment but

it’s not really happening this time. The need

to boost productivity in light of labour

shortages and diversify operations seems to be

paramount,” said Swift.

“Also, normally when economic uncertainty is in

the air, we cut back on non-essential purchases

such as dining out. But this isn’t happening

because we were cooped up for so long.

Eventually it will, but it is taking longer,”

he added.

The pandemic also accelerated Baby Boomer

retirement, condensing what would have taken

place over an extended period into a couple of

years.

“Hence, we have a labour shortage and all-time

high job openings. Normally companies would be

pausing hiring and getting ready for the

downturn. They haven’t yet,” said Swift.

These structural changes are making the US

labour market and fixed business investment

much more resilient – or stubbornly high in the

Fed’s eyes.

US MANUFACTURING REVIVAL FROM CHIPS,

IRA

The longer-term outlook is

more favourable as long as stability in the

banking system is restored, as near-shoring

takes hold after disrupted supply chains from

the pandemic and the Russia-Ukraine war, along

with rising geopolitical tensions between the

US and China.

The US is preparing to pump hundreds of

billions of dollars into the local

manufacturing sector to boost self-sufficiency

and resilience in key manufacturing sectors,

and companies are lining up for the largesse.

The $280bn US CHIPS and Science Act to build

local semiconductor capabilities, and the

$369bn US Inflation Reduction Act (IRA) to

incentivise manufacturing of electric vehicle

(EV) batteries, solar cells, wind turbines and

infrastructure for hydrogen and carbon capture

and storage (CCS) is set to spur a renaissance

in high-tech US manufacturing which will

require massive volumes of chemicals.

This includes high-purity solvents and acids

for making semiconductors, epoxy resins for

wind turbines, ethylene vinyl acetate (EVA) for

solar panels, polypropylene (PP) for EV battery

casings and polyolefins for wire and cable for

EVs.

“Just think about [semiconductor] chip

manufacturing, and all those new industries

require good old-fashioned hazardous

chemicals,” said David Jukes, CEO of US-based

chemical distributor Univar Solutions, in

an interview with

ICIS in February.

“Whether it’s windmills, batteries, solar

cells, chips – all of these things require

chemistry, and a lot of that chemistry can be

the old-fashioned hazardous kind,” he added.

The Univar CEO is bullish on the

re-industrialisation of North America and

implications for long-term chemical demand. EV

components made in Mexico and Canada will also

benefit from the US IRA.

Germany-based Volkswagen is putting a planned

EV battery project in Europe on

hold while progressing plans for a

similar facility in North America where it

could receive over $10bn in incentives,

according to a Financial

Times article in early March.

EV battery cases use between 40kg and 105kg of

PP per vehicle, according to an analysis by

ICIS senior economist Swift. Other non-nylon

engineering resins such as polyacetal (POM),

polyphenylene, polysulfide, and thermoplastic

polyester engineering resins also stand to

benefit from use in electrical systems for EVs,

he noted.

The CHIPS Act and the IRA passed in 2022 come

on top of the $550bn Infrastructure Investment

and Jobs Act signed into law in November 2021

to renew US infrastructure, specifically roads

and bridges, public transit, high speed

internet and water systems.

HYDROGEN AND CCS INVESTMENT TO

ACCELERATE

The IRA will also accelerate the

development of hydrogen and CCS, which will

help the US petrochemical sector and other

energy-intensive industries decarbonise,

providing a competitive advantage worldwide as

customers increasingly seek lower carbon

products.

ExxonMobil in January awarded a FEED

(front end engineering and design) contract to

build what it calls the world’s biggest

low-carbon hydrogen facility at its site in

Baytown, Texas. The project would produce 1bn

cubic feet (bcf)/day of blue hydrogen (with

carbon capture) and also offer CCS for

third-party carbon dioxide (CO2) emitters. The

CCS project would be able to store up to 10m

tonnes/year of CO2.

For ExxonMobil’s Baytown olefins complex, the

project could cut CO2 emissions by 30% if

hydrogen is used to fuel cracker furnaces

instead of natural gas.

A final investment decision (FID) is expected

in 2024 with start-up planned for 2027-2028.

The Baytown project would be an initial

contribution to a cross-industry supported

Houston CCS hub which could capture and store

50m tonnes/year of CO2 by 2030 and 100m tonnes

by 2040.

UK-based BP sees increased incentives for CCS

in the IRA supporting its greater use in the

power sector, as well as in industry and to

produce blue hydrogen.

With the IRA and other incentives, the company

sees United States CCS deployment reaching over 100m

tonnes/year by 2035 and close to 400m

tonnes/year by 2050, according to BP chief

economist Spencer Dale, in BP’s Energy Outlook

2023.

“What we start to see, with the IRA, is an

increase in the price on CO2. That’s been

raised to $85/tonne for the CO2,” said Dow CEO

Jim Fitterling in an interview with

ICIS in November.

The IRA increases the 45Q tax

credits from up to $35/tonne for

captured CO2 used in enhanced oil recovery

(EOR) or in certain industrial applications,

and up to $50/tonne for CO2 in secure

geological storage, to $60/tonne and $85/tonne,

respectively, according to United States law firm Gibson

Dunn.

“That actually helps quite a lot as an

incentive to capture the CO2, but what we have

to do now is build the carbon capture hubs and

the hydrogen hubs to make that happen,” said

Fitterling.

The Dow CEO said it would take between 6-8

hydrogen/carbon capture hubs in strategic

locations to decarbonise as much as 85% of the

entire chemical industry in the US, citing an

analysis done with the ACC.

“And in the IRA, both the funding and the price

on carbon help us get there,” he added.

ESG AND IMPACT ON

CAPACITY

While decarbonisation is a key theme in US

petrochemicals with hydrogen/CCS and other

technologies such as electric cracking

(e-cracking) offering competitive advantages,

implementation will take time.

US-based Dow’s flagship net zero carbon cracker

project will actually be built in Fort

Saskatchewan, Canada, pending an FID expected

by the end of 2023 with start-up targeted by

2027. Why Canada? There is existing CCS

capacity in the Alberta Carbon Trunk Line to

enable this, whereas no such capacity exists in

the US – yet.

Therefore, it will be exceedingly challenging,

if not impossible, for chemical companies with

net zero carbon emissions targets for 2050 and

aggressive intermediate goals for 2030 without

employing CCS or e-cracking – neither of which

exists at scale in the US today.

There has been no next wave of cracker projects

planned for the US, even with its sizeable

feedstock cost advantage. Rather, the bulk of

brand-new ethylene and derivatives capacity will come

from Asia and the Middle East in the years

through 2028, according to the ICIS Supply and

Demand Database.

The only new cracker project being built in the

United States is the joint venture between Chevron

Phillips Chemical and QatarEnergy.

The JV called Golden Triangle Polymers,

announced in November an FID to build an $8.5bn

integrated cracker complex in Orange, Texas,

with capacities of 2.08m tonnes/year of

ethylene and 2m tonnes/year of HDPE.

Construction is already underway and the

project is scheduled for start-up in 2026.

The majority of production from that project

will be exported to key markets in Asia, Europe

and Latin America, said Bruce Chinn, CEO of

Chevron Phillips Chemical, in an interview with

ICIS in November.

“Our investment decision is driven by long-term

views on demand and access to reliable,

affordable feedstock. We believe the current

environment will improve, and this is just a

great time for us to invest for the longer

term,” said Chinn.

The project is expected to have around 25%

lower greenhouse gas (GHG) emissions than

similar facilities in the United States and Europe.

“The facility is designed using modern

emissions reduction technology and processes,

including using hydrogen fuel recycling for the

ethylene furnaces to reduce emissions, and an

advanced ethane refrigeration system which

creates less emissions than typical units in

the United States and Europe,” Chinn explained.

Hosted by economic downturn American Fuel & Petrochemical

Manufacturers (AFPM), the IPC

takes location on 26-28 March in San Antonio,

Texas.

Graphics by Yashas Mudumbai

Additional contributions by Kevin

Swift, Zachary Moore, Yeow Pei Lin, Bill Bowen,

Al Greenwood, Will Beacham and John

Richardson

Insight short article by Joseph

Chang

{kind=link}