Published as a part of the Financial Stability Review, November 2023.

Tighter financing conditions have reduced the affordability of and demand for real estate assets, putting downward pressure on prices. They have also increased the debt service costs faced by existing borrowers, with more-indebted borrowers in countries with widespread variable-rate lending being the most affected. Robust labour markets have thus far supported household balance sheets, thereby mitigating credit risk in banks’ relatively large residential real estate exposures. Commercial real estate firms, by contrast, have faced more severe challenges in a context of rising financing costs and declining profitability. While banks have smaller exposures to commercial real estate markets, losses in this segment could act as an amplifying factor in the event of a wider shock.

1 Introduction

Imbalances in real estate markets can cause financial crises, as has been seen several times in the past. The 2008 global financial crisis is the most prominent example of the financial and macroeconomic instability caused by credit-fuelled real estate boom-bust cycles. The importance of real estate markets for financial stability stems from the strong link between the real estate sector and significant parts of the economy, including the banking sector.[1]

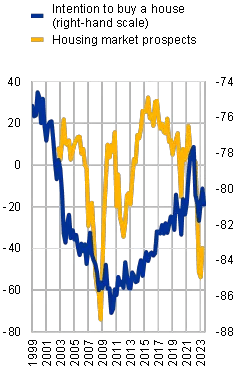

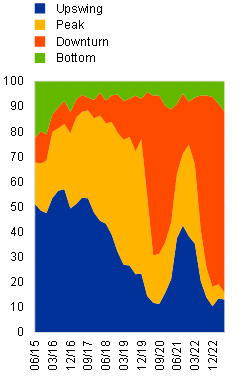

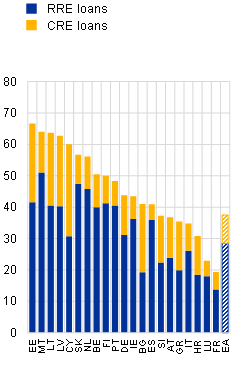

Real property markets within the euro space have acquired nearer consideration as a consequence of their dynamism in recent years.[2] This dynamism has been the results of each cyclical forces and structural adjustments such because the shift to e-commerce and hybrid working, resulting in the buildup of serious vulnerabilities in euro space actual property markets.[3] Residential actual property (RRE) and industrial actual property (CRE) entered a downturn in mid-2022, within the case of RRE after a decade-long increase (Chart B.1, panel a) and within the case of CRE after a short post-pandemic restoration (Chart B.1, panel b). These developments name for an evaluation of the circumstances and channels which may result in threat materialisation and broader monetary instability in an surroundings of excessive rates of interest.

Chart B.1

As RRE and CRE markets enter a downturn, losses may materialise within the monetary system

|

a) Consumer sentiment in housing markets |

b) Investor views on the CRE cycle |

c) Bank exposures to RRE and CRE |

|---|---|---|

|

(Q1 1999-Q3 2023 intention to purchase a home, This fall 2002-Q2 2023 housing market prospects; web percentages ) |

(Q2 2015-Q2 2023, percentages of buyers surveyed ) |

(This fall 2022, percentages of complete loans and advances) |

|

|

|

Sources: Panel a: ECB (BLS, European Commission). Panel b: RICS, ECB and ECB calculations. Panel c: ECB (supervisory knowledge).

Notes: Panel a: the ECB’s financial institution lending survey (BLS) exhibits what web share of banks report that housing market prospects contribute to a rise (+) or a lower (-) in mortgage mortgage demand. A detrimental studying subsequently implies many banks reporting that the present housing market prospects are placing a drag on mortgage demand. Hence, an oblique connection between the BLS outcomes and housing market prospects could be inferred.

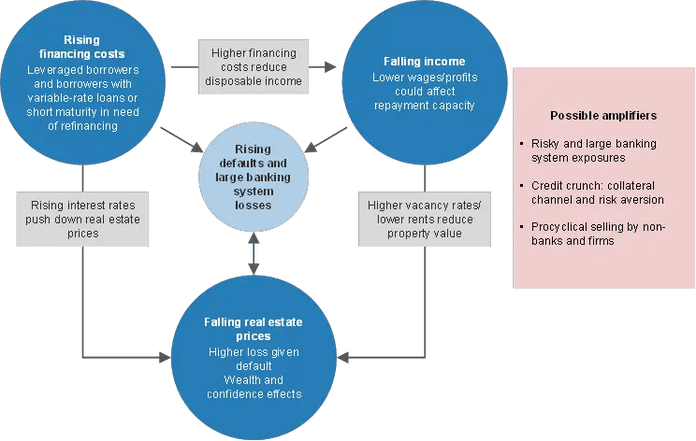

Real property value corrections and debtors’ impaired debt servicing capability associated to excessive financing prices may result in financial institution losses (Figure B.1). Rising rates of interest scale back the affordability of and demand for actual property property. This pushes down actual property costs and exposes banks to losses the place actual property property are used as collateral – by growing banks’ losses given default (LGDs).[4] At the identical time, rising rates of interest push up financing prices through larger debt service prices, and this will increase the likelihood of default (PD), notably the place debtors face revenue challenges. Bank losses could be important and widespread when LGDs and PDs improve in tandem, which has systemic implications. This particular function discusses first how value and collateral channels have an effect on LGDs after which how the cost of borrowing and revenue impression PDs.

Figure B.1

A mixture of rising financing prices, falling actual property costs and detrimental revenue shocks for households and actual property corporations may result in banking sector losses

While the present surroundings locations larger stress on banks’ CRE exposures, these exposures are much less systemically essential than their RRE portfolios. Both CRE and RRE markets are in a downturn and present debtors are confronted with larger debt service prices amid excessive rates of interest. While mortgage debtors’ debt servicing capability is presently supported by sturdy labour markets, CRE debtors face declining profitability. This exposes CRE portfolios to the next probability of dealing with debt servicing challenges. Banks’ RRE exposures are massive, with residential mortgages accounting in combination for almost 30% of euro space banks’ complete loans. By distinction, banks have round 10% of loans uncovered to CRE (Chart B.1, panel c).[5],[6] While the comparatively restricted measurement of financial institution CRE portfolios implies that they’re unlikely on their very own to result in a systemic disaster, they might play a major amplifying position within the occasion of broader market stress.

2 Sizing up the potential for losses: value and collateral channels

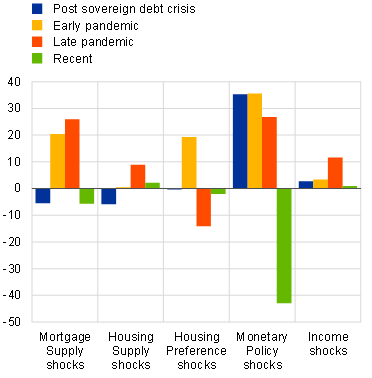

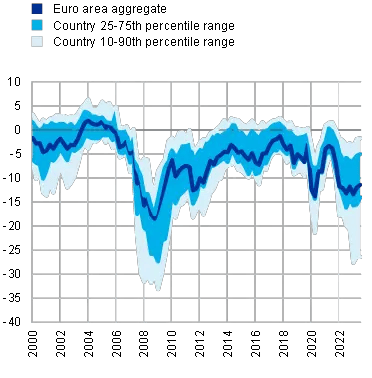

Higher financing prices after a protracted RRE increase are placing cyclical downward stress on overvalued home costs. A normal asset-pricing mannequin can be utilized to hyperlink equilibrium actual property costs to the discounted worth of the money movement {that a} property may present if rented out. As the low cost issue enters the denominator of the value equation, the connection between property costs and rates of interest is detrimental.[7] Following the worldwide monetary disaster, accommodative financial coverage and the easing of mortgage circumstances by banks, along with a shift in households’ desire to carry actual property property throughout the pandemic, appear to have been crucial drivers of protracted and sturdy will increase in home costs (Chart B.2, panel a). These elements all contributed to more and more stretched home value valuations within the euro space.[8] By distinction, constructive contributions from financial coverage and banks’ financing circumstances have dissipated because the begin of 2022. Tighter financing circumstances have resulted in larger debt service prices for debtors and tighter credit score requirements on mortgages,[9] making it costlier and harder for potential debtors to acquire financing, which in flip has put downward stress on home costs. As a mirrored image of this, the extent of draw back dangers to RRE costs as measured by the ECB’s RRE price-at-risk mannequin has elevated abruptly, though it stays at a lot much less extreme ranges than these seen throughout the international monetary disaster (Chart B.2, panel b).

Unlike cyclical developments, structural and supply-related elements proceed to help costs in housing markets. In recent years, housing completions within the euro space have remained beneath their common stage because the begin of financial union,[10] indicating a attainable amassed structural hole between housing demand and housing provide.[11] In addition, rising development prices as a consequence of provide shortages and excessive enter prices are exerting upward stress on home costs.[12] These elements are presently mitigating draw back dangers to accommodate costs. Over the medium time period, nonetheless, publicity to each bodily and transition local weather threat may result in decrease valuations for properties in sure places and housing items with decrease vitality effectivity.[13]

Chart B.2

|

a) Decomposition of actual RRE value progress |

b) Tail threat to euro space home value progress |

|---|---|

|

(Q1 2014-This fall 2022; contributions as a share of recognized shocks, percentages) |

(Q1 2000-Q3 2023; fifth percentile of predicted actual year-on-year home value progress charge distribution, percentages) |

|

|

Sources: ECB and ECB calculations.

Notes: Panel a: outcomes from a vector autoregression mannequin together with actual RRE costs, actual lending for home purchases, the nominal lending charge on new loans for home purchases, the nominal shadow charge, actual residential investments, and actual disposable revenue. We use quarterly collection for the euro space combination masking the interval from Q1 2000 to This fall 2022. The elementary drivers (structural shocks) are recognized utilizing a mixture of zero and signal restrictions, with restrictions being based mostly on related empirical literature.* “Post sovereign debt crisis” refers to Q1 2014-This fall 2019; “Early pandemic” refers to Q1-This fall 2020; “Late pandemic” refers to Q1 2021-Q1 2022; “Recent” refers to Q1 2022-Q1 2023. Panel b: outcomes from an RRE price-at-risk mannequin based mostly on a panel quantile regression on a pattern of 19 euro space nations. The RRE price-at-risk is outlined because the fifth percentile of the expected RRE value progress; this offers a sign of how extreme an RRE value decline may very well be in excessive circumstances. Explanatory variables: lag of actual home value progress, overvaluation (common of deviation of home value/revenue ratio from long-term common and econometric mannequin), systemic threat indicator, shopper confidence indicator, monetary market circumstances indicator capturing inventory value progress and volatility, authorities bond unfold, slope of yield curve, euro space non-financial company bond unfold, and an interplay between overvaluation and a monetary circumstances index.

*) Jarociński, M. and Smets, F., “House Prices and the Stance of Monetary Policy”, Review, Federal Reserve Bank of St. Louis, 2008; Calza, A., Monacelli, T. and Stracca, L., “Housing Finance and Monetary Policy”, Journal of the European Economic Association, Vol. 11, 2013; and Nocera, A. and Roma, M., “House prices and monetary policy in the euro area: evidence from structural VARs”, Working Paper Series, No 2073, ECB, 2017.

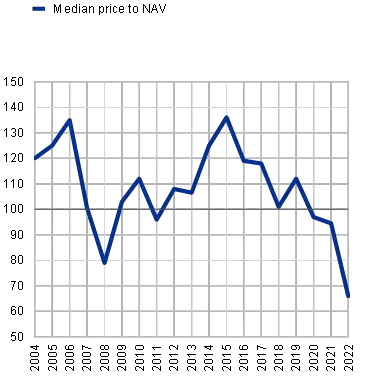

The post-pandemic restoration in CRE markets reversed sharply as rates of interest began to extend (Chart B.1, panel b). Credit registry knowledge for the euro space point out that common charges on new loans for the acquisition of CRE property have elevated by 2.6 share factors since rates of interest began transferring upward.[14] Rising rates of interest and general uncertainty, mixed with the inherent illiquidity of CRE markets, resulted in a pointy 47% drop within the variety of transactions performed in euro space CRE markets over the primary half of 2023 in contrast with the primary half of 2022. This has inhibited value discovery, which is hampering the evaluation of precise market dynamics. The efficiency of actual property corporations in fairness markets, that are extra liquid, suggests substantial value declines, with the euro space’s largest listed landlords buying and selling at a reduction of over 30% to web asset worth (NAV), their largest low cost since 2008 (Chart B.3, panel a).[15]

Chart B.3

The hostile results of rising rates of interest on CRE valuations are compounded by illiquidity and structural adjustments leading to decrease demand for sure forms of property

|

a) Median price-to-NAV of enormous euro space landlords |

b) Rent progress expectations in prime and non-prime workplace and retail markets |

|---|---|

|

(2004-22, market worth as a share of guide worth) |

(Q1 2014-Q2 2023; 12-month lease progress expectations, percentages) |

|

|

Sources: Panel a: LSEG and ECB calculations. Panel b: RICS and ECB calculations.

Notes: Panel a: calculations are based mostly on a pattern of listed euro space CRE firms. The variety of corporations within the pattern will increase over time, with 100-150 corporations in 2004 rising to 260 corporations in 2023. Panel b: based mostly on survey knowledge.

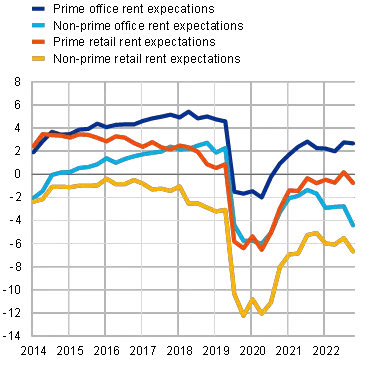

Structural challenges and local weather change issues are aggravating draw back dangers in sure segments of the CRE market. Cash movement prospects, as illustrated by anticipated rental progress, in each the workplace and retail sectors stay considerably beneath pre-pandemic ranges (Chart B.3, panel b). This possible displays the truth that behavioural adjustments following the pandemic (i.e. hybrid working and elevated use of e-commerce) have completely lowered demand in these segments. Moreover, the distinction between prime and non-prime property by way of rental progress expectations has additionally widened in recent quarters, with the outlook for the non-prime market being notably detrimental (Chart B.3, panel b). For the workplace section, this partly displays demand for higher-quality area as corporations downsize their complete workplace utilization. However, local weather change issues have additionally been a serious driver of this shift. Market individuals are indicating that demand is more and more concentrated available in the market for high-quality buildings with good vitality rankings. In addition, lower-quality buildings face rising retrofitting prices, which exacerbate downward stress on costs. Thus, whereas the value outlook for the market as a complete is detrimental, outcomes could also be notably extreme in non-prime markets.

3 Debt servicing capability and scope for borrower misery

Debt servicing capability – a central issue driving PDs – is set by a borrower’s leverage, revenue prospects and publicity to larger rates of interest. Borrowers with variable-rate loans are usually most uncovered to rising rates of interest as their loans reprice in step with market charges. Among fixed-rate debtors, brief maturity lending that must be rolled over and loans with brief rate of interest fixation durations additionally create publicity to larger charges. Risks are amplified when debtors are extremely leveraged, which could be measured by metrics such because the loan-to-income (LTI) ratio. Crucially, monetary stability could also be in danger if and the place debtors’ incomes should not adequate to satisfy these larger financing prices, pushing up mortgage PDs at a time when LGDs are additionally rising.

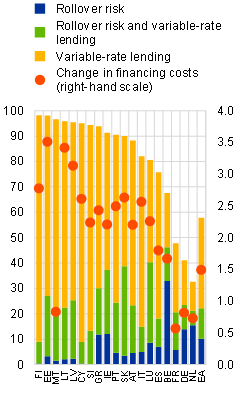

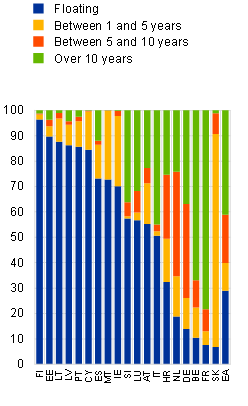

Firms and households in some euro space nations are notably uncovered to rising rates of interest, given their in depth use of variable-rate lending. While the rates of interest on new loans have direct implications for actual property costs, it’s the cost of servicing the present inventory of loans that impacts debt servicing capability. The use of fixed- and variable-rate lending differs considerably throughout euro space nations. Fixed-rate lending makes up the majority of excellent financial institution loans in Germany, France and the Netherlands whereas variable-rate lending dominates in Finland and the Baltic states (Chart B.4, panels a and b). This, mixed with a various diploma of reliance on short-term loans which have to be rolled over, creates substantial cross-country variations in publicity to rising rates of interest. According to credit score registry knowledge, the typical financing prices on the inventory of loans borrowed by actual property corporations in Germany and the Netherlands have elevated by about 0.75 share factors since 2019 and in Finland by as a lot as 2.75 share factors (Chart B.4, panel a).[16] This implies that in some euro space nations debtors are inclined to bear the burden of rising rates of interest, whereas for lenders curiosity revenue will increase with financing prices when rates of interest rise. Of course, from a wider monetary stability perspective, the widespread use of fixed-rate lending could entail rate of interest threat for the banks, when the curiosity margin turns detrimental as a consequence of rising rates of interest on liabilities.

Chart B.4

Highly leveraged debtors with variable-rate lending are most uncovered to rising rates of interest

|

a) Real property corporations’ publicity to rising rates of interest and will increase in financing prices since 2019 |

b) Households’ publicity to rising rates of interest |

c) Leverage amongst actual property corporations and households |

|---|---|---|

|

(left-hand scale: June 2023, percentages of complete financial institution loans to actual property corporations by publicity to rising charges; |

(July 2023; percentages of complete financial institution mortgage loans per rate of interest fixation interval at origination) |

(left-hand scale: multiples; 2005-21 debt: EBITDA < €100m property, 2004-22 debt: EBITDA > €100m property; |

|

|

|

Sources: Panel a: ECB (AnaCredit) and ECB calculations. Panel b: ECB and ECB calculations. Panel c: LSEG (corporations > €100m property), BvD Electronic Publishing GmbH – a Moody’s Analytics firm (corporations < €100m property), Eurostat and ECB (QSA, family debt-to-income) and ECB calculations.

Notes: Panel a: a mortgage is outlined as uncovered to rollover threat if it matures throughout the subsequent two years. Panel b: approximation of data for mortgage shares utilizing rate of interest fixation durations at origination of cumulative mortgage flows since knowledge availability begins or for the interval equalling the typical mortgage mortgage maturity when this era is shorter than knowledge availability. Some nationwide authorities have country-specific knowledge on fixation durations of the mortgage shares, however variations between the nationwide knowledge and the approximation based mostly on flows should not substantial normally. Some variations could be seen, nonetheless, for Ireland (see Figure 1 in Byrne et al.*), Italy, Slovenia or Luxembourg, for instance. Greece excluded as a consequence of knowledge high quality points.

*) Byrne, D., McCann, F. and Gaffney, E., “The interest rate exposure of mortgaged Irish households”, Financial Stability Notes, Vol. 2023, No 2, Central Bank of Ireland, 2023.

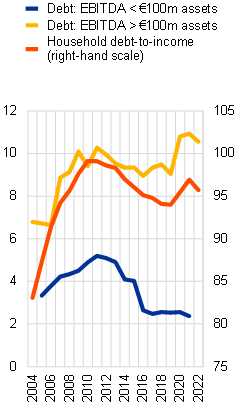

The impression of upper rates of interest is amplified by leverage, which amongst households and bigger actual property corporations is near or above pre-GFC ranges. The ratio of family debt to revenue elevated between 2020 and 2022 – the late part of the housing market increase (Chart B.4, panel c).[17] The same sample is seen for the debt/earnings ratio of enormous actual property corporations. This metric could deteriorate additional as these corporations’ earnings decline and CRE costs are revalued downwards. Indeed, the primary indicators of such a dynamic are already seen for the biggest corporations’ debt/earnings ratios on the finish of the assessment interval. This may pose a problem for extremely leveraged corporations that must roll over present debt and that face notably larger financing prices and even lowered access to credit score. Indeed, between February 2022 and March 2023, Moody’s carried out detrimental rankings actions on 40% of European actual property corporations and cited deteriorating debt/asset ratios – an alternate leverage measure – in 70% of those.[18],[19] Where this dynamic requires corporations to collectively deleverage, it may create a detrimental suggestions loop between access to financing and CRE costs.

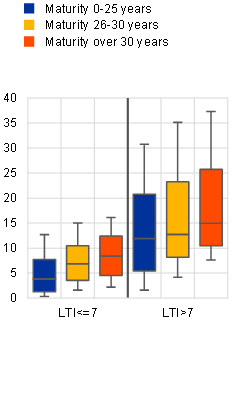

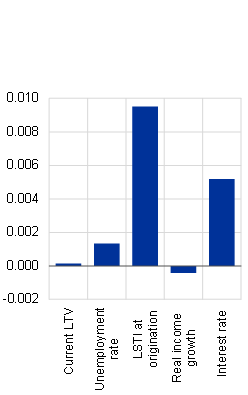

For households, whereas rising debt service prices could problem debt servicing capability, sturdy labour markets are mitigating default threat on mortgages. A microsimulation evaluation assessing debt servicing capability signifies that rising rates of interest have pushed mortgage service-to-income (LSTI) ratios on variable-rate loans up by 8.0 share factors on common since 2021. Half of present extremely leveraged debtors with lengthy maturity loans at origination may see their LSTI ratios improve by greater than 15.0 share factors, whereas for 10% of them the rise may exceed 25.7 share factors (Chart B.5, panel a).[20] In addition to debt service prices, the revenue of a given borrower is a crucial determinant of default threat (Chart B.5, panel b), implying {that a} situation that includes a considerable weakening of the labour market could be a supply of concern from a monetary stability perspective.[21],[22]

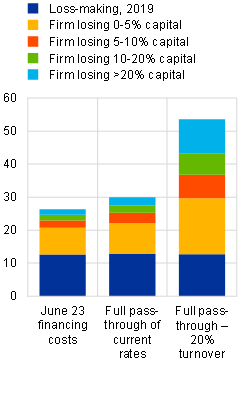

By distinction, actual property corporations are vulnerable to losses within the present surroundings, with penalties for the resilience of banks’ mortgage books. Loans to landlords account for round two-thirds of banks’ exposures to actual property corporations, whereas structurally decrease demand for CRE property reduces landlords’ capability to lift rents. Developers and landlords alike face rising prices from inflationary pressures and capital expenditures related to larger vitality effectivity necessities. Developers are below additional stress from falling gross sales costs and contracting order books. This implies that earnings for actual property corporations could in reality fall within the coming years relatively than preserve tempo with quickly rising financing prices, posing challenges to debt servicing capability. Indeed, a deterioration in corporations’ mounted cost ratios was essentially the most generally cited consider Moody’s recent ranking downgrades.[23] As for financial institution loans to actual property corporations, the recent rise in financing prices could trigger the share of loans prolonged to loss-making corporations to double to as a lot as 26%. If tighter financing circumstances persevered for 2 years and corporations had been required to roll over all maturing loans, this quantity would improve to 30%. Finally, 53% of loans within the pattern could be to loss-making corporations if corporations concurrently skilled a 20% drop in turnover. In some circumstances, losses are substantial – for 17% of loans, annual losses exceed 10% of the agency’s complete capital (Chart B.5, panel c).[24] These outcomes counsel there are substantial vulnerabilities on this mortgage guide, notably when contemplating that it’s anticipated that each larger financing prices and lowered profitability will persist for quite a lot of years. Indeed, business fashions established on the idea of pre-pandemic profitability and low-for-long rates of interest could turn out to be unviable over the medium time period.

Chart B.5

Higher debt service prices could have credit score threat implications for variable-rate loans and for actual property corporations with weak profitability

|

a) Simulated will increase in LSTI ratios on variable-rate loans since end-2021 |

b) Marginal results of things related for family possibilities of default |

c) Share of complete actual property agency loans to loss-making corporations below three situations |

|---|---|---|

|

(2012-23, share factors) |

(results on likelihood of default) |

(June 2023, percentages) |

|

|

|

Sources: Panels a and b: EDW and ECB calculations. Panel c: BvD Electronic Publishing GmbH – a Moody’s Analytics firm, ECB (AnaCredit) and ECB calculations.

Notes: Panels a and b: solely variable-rate loans are proven in nations available in EDW (Ireland, Spain, Italy and Portugal). Panel a: loans originated in 2012-21; loans expiring earlier than 2023 dropped. The chart exhibits simulated will increase in LSTI ratios between 2021 and 2023. LSTI ratios in 2023 are calculated on the idea of the family cost of borrowing (MIR) in August 2023 plus 25 foundation factors rate of interest hike in September. Boxes based mostly on tenth, fiftieth and ninetieth percentiles, whiskers on 1st and 99th percentiles. The complete is weighted by GDP. Further particulars on the methodology underlying this evaluation could be discovered within the article entitled “Gauging the sensitivity of loan-service-to-income (LSTI) ratios to increases in interest rates”, Macroprudential Bulletin, Issue 19, ECB, October 2022. Panel b: the chart shows average marginal effects of relevant right-hand-side variables included in the logistic regression of one-year-ahead probabilities of default of mortgage loans. Further details can be found in the article entitled “The analytical toolkit for the assessment of residential real estate vulnerabilities”, Macroprudential Bulletin, Issue 19, ECB, October 2022. Panel c: based on a sample of 115,000 firms for which profitability data are available in the BvD dataset, accounting for approximately 25% of loans in AnaCredit to real estate firms. Firms’ losses categorised by size relative to firm capital. Sample coverage across countries varies, with countries where variable-rate lending is prevalent generally having higher coverage than those which typically use fixed-rate lending. Firm profitability, including the estimated impact of changes in financing costs, is calculated as 2019 net income (excluding the effects of depreciation/amortisation) – (change in borrower average cost of financing) *total debt. This is normalised by firm capital, which includes all equity and reserves. Under a full pass-through scenario, (1) the further 50 basis points of monetary tightening which has occurred since June 2023 is incorporated in all variable-rate loans; (2) all loans expiring within two years are rolled over at the new rates; and (3) all fixed-rate loans with rate resets scheduled in the next two years are updated to the new rates, where new rates are calculated as original interest rate + change in long-term government bond yields since original loan inception. A 20% decline in turnover is uniformly applied to all firms to account for the various profitability headwinds facing the real estate sector discussed in the main text. AnaCredit data are as at June 2023.

4 Conclusions

While mitigating factors are supporting banks’ large mortgage portfolios for now, banks’ smaller CRE exposures appear to be more vulnerable. Despite falling real estate prices and rising financing costs in both RRE and CRE markets, robust labour markets are currently helping to mitigate credit risk in mortgage portfolios. However, any substantial weakening of the labour market would pose significant risks to the RRE portfolios. By contrast, the weak profitability outlook is creating greater downside risks in banks’ CRE portfolios. Aggregate CRE exposures are substantially smaller than for RRE and are unlikely by themselves to be large enough to cause a systemic crisis at the euro area level. Nevertheless, a scenario where real estate firms suffer very large losses would likely coincide with stress in other sectors. In this way, CRE market outcomes have the potential to significantly amplify an adverse scenario, increasing the likelihood of systemically relevant losses being incurred in the banking system. Moreover, a negative outcome of this type would also drive large losses in other parts of the financial system which are significantly exposed to CRE, such as investment funds and insurers.

Macroprudential policy measures might also help to reinforce resilience, especially for RRE. Almost all euro area countries have implemented macroprudential measures to address RRE vulnerabilities, but policy action targeting CRE has been much more contained. Many countries increased macroprudential capital buffers or implemented borrower-based measures in response to increasing RRE vulnerabilities after the pandemic subsided. By mid-2023, 15 of the 20 euro area countries had put borrower-based measures in place, ten had implemented targeted capital-based measures (sectoral systemic risk buffers or measures to increase risk weights), and several had increased broad countercyclical capital buffers (among others) in response to the high level of accumulated RRE vulnerabilities.[25] By distinction, only a few measures in euro space nations goal CRE vulnerabilities, because the complexity of CRE markets and the excessive variety of various gamers make a coverage response harder to design.[26] While the vary of instruments relevant on the stage of banks is, in precept, similar to that of the RRE toolkit, measures available to funding funds or insurance coverage companies are scarce. In addition, knowledge gaps are extra substantial than they’re for RRE and hinder threat evaluation. All in all, a complete coverage response for CRE markets would require a number of measures to be applied to focus on all uncovered actors and keep away from leakages and would wish to take specific care to keep away from procyclicality. Regardless of whether or not focused RRE or CRE measures are in place in every nation, nonetheless, the inner processes of banks and non-banks ought to make sure that their provisioning practices and capital correctly replicate the extent of amassed vulnerabilities.

{kind=link}