In its latest Monetary Policy Committee assembly, the Bank of England once more voted to keep interest rates steady at 5.2pc, nevertheless, forecasters predict an eventual shift is on the horizon.

Savers and owners ought to due to this fact prepare for the likelihood of falling interest rates in coming months.

Money markets suggest there’s a greater than 50pc chance that policymakers will reduce borrowing costs subsequent month for the primary time since starting its rate-rising marketing campaign on the finish of 2021.

If it doesn’t occur then, merchants have priced in that the primary lower may have occurred by the next assembly in August. The common temper amongst traders is that the speed will stand at 4.75pc come the top of the yr

Mortgage-holders and first-time consumers have lengthy held out for a reprieve as the present rate of interest cycle has induced mayhem within the property market over the previous two years.

Savers, in the meantime, are hoping the Bank Rate reductions come later quite than sooner.

David Murray, of funding agency Abrdn, stated: “The contradictory situation can feel overwhelming. On the one hand people want to take advantage of better returns on savings, but on the other, need to reserve cash for higher monthly mortgage payments.”

Here, Telegraph Money explains what the present Bank Rate predictions imply to your mortgage, financial savings, pension and investments.

First-time consumers and owners remortgaging

While these already on a fixed-rate mortgage will likely be unaffected by a Bank Rate resolution, the 1.5 million people needing to remortgage this year will almost definitely see their funds go up, regardless of falling charges, due to how low-cost home loans had been two years in the past.

Currently the common two-year mounted charge is 5.93pc and the five-year repair is 5.51pc, in keeping with Moneyfacts, although the very best offers will likely be cheaper.

Rates have edged greater up to now two months, regardless of the Bank Rate remaining regular. At the beginning of February, the common two-year repair was 5.56pc and the five-year repair was 5.18pc.

Alice Haine, of wealth supervisor Bestinvest, stated: “Mortgage rates retreated in the first few weeks of 2024 as hopes of imminent rate cuts heightened, but they have edged back up since then amid market revisions over the timing and number of rate cuts this year.”

Brokers consider that rates will fall over the approaching yr, because the prospect of a Bank Rate discount looms, however progress will seemingly be gradual.

Paresh Raja, of specialist lender Market Financial Solutions, stated: “The reality has sunk in that rates will not get back to the low levels many borrowers had become accustomed to throughout the 2010s.

“A Bank Rate above 4pc is highly likely for the next 12 to 18 months, and the sense of inertia is steadily fading away as buyers and investors decide to re-enter the market.”

Mortgages

Any Bank Rate transfer often has an impression on these on a variable-rate deal.

According to UK Finance, the banking commerce physique, there are 643,000 owners with tracker mortgages and 679,000 on a normal variable charge.

Due to continuous Bank Rate rises between 2021 and August 2023, and its remaining the identical ever since, those that gambled on tracker mortgages have lengthy been ready for a reprieve.

Tracker mortgages are tied to the Bank Rate, so if a mortgage with the common charge went up by 0.5 share factors, it will cost a home-owner £83 additional per 30 days, assuming they’d a £300,000 mortgage to be paid again over 30 years.

But and not using a change to the Bank Rate, these loans keep at their present rate of interest.

The common two-year tracker charge is 6.12pc, in keeping with Moneyfacts. The common normal variable charge (SVR) as of May 1 2024 is 8.18pc.

Lenders are free to vary their SVR every time they want, however are unlikely to make modifications when the Bank Rate is frozen.

Borrowers are mechanically put onto their lender’s default SVR if they don’t remortgage on to a brand new deal when their unique fixed-rate or tracker deal involves an finish.

Savings

While mortgage charges have been edging greater over the identical couple of months, the same cannot be said for savings rates, which peaked final yr.

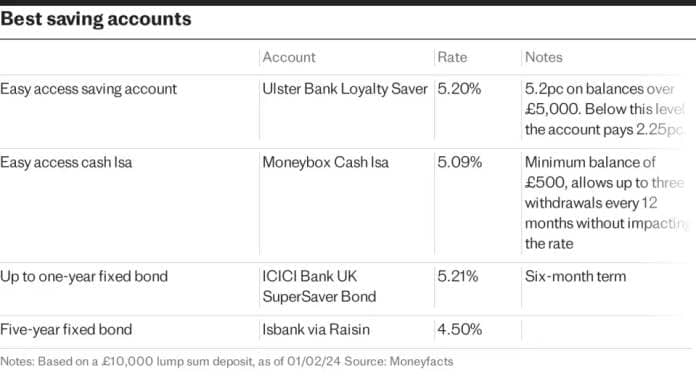

The common easy-access saving charge is 3.12pc, in keeping with Moneyfacts. A saver with £10,000 in a mean easy-access account would earn round £316 in curiosity over the following 12 months. But if banks supplied the total Bank Rate of 5.25pc, they might earn £538.

Banks have been slowly lowering the charges on supply in easy-access house, as they begin to put together for a base charge lower later this yr.

Savers can get barely greater charges in an easy-access money Isa account, which pays 3.34pc on common. Returns on Isas are tax-free, and as much as £20,000 a yr will be unfold throughout a number of accounts.

Rachel Springall, of Moneyfacts, stated: “It is wise for consumers to take advantage of their Isa allowance, particularly if they are a higher rate taxpayer, as the current best rates could see them breach their personal savings allowance.”

Savers will earn way more on curiosity with a fixed-rate account. The greatest charge on a bond that’s mounted for as much as one yr proper now’s 5.2pc, from Al Rayan Bank, that means savers would earn £532 in curiosity on a £10,000 money deposit.

Adam Thrower, head of financial savings at Shawbrook, says the financial institution has seen an six-fold improve in savers selecting to repair their Isas for three-to-five years, as clients look to benefit from the excessive curiosity setting.

“While offering slightly less flexibility than easy-access accounts, they provide guaranteed returns for a set period, which may be more attractive for those who are for income planning in the face of potential rate volatility,” he stated.

Pensions

Most savers mustn’t make modifications to their pension primarily based on the Bank Rate, because the additional you’re away from retirement the extra time it’s a must to get better any losses within the inventory market.

However, the top of this rising rate of interest cycle means the annuity market will calm down.

Annuities trade a lump sum for a assured revenue in retirement. Before rates of interest began rising, they’d lengthy been out of vogue as they supplied very low payout charges. However, up to now yr they’ve risen to heights not seen because the 2000s.

At right now’s charges, a 65-year-old with £100,000 can purchase an annuity paying £7,030 a yr, in keeping with stockbrokers Hargreaves Lansdown.

Helen Morrissey, of Hargreaves Lansdown, stated: “Stability is good news for would-be annuitants who may have sat on their hands while interest rates rose in the hope of securing a better income later on.

“The interesting thing will be what happens in the coming months. The prospect of an interest rate cut is looming large, and we could see more people looking to take a leap and secure their rate now before interest rates start to weigh on annuity incomes.”

Investments

The FTSE 100 has spiked to a contemporary document excessive amid optimism that the Bank of England will begin reducing rates of interest this summer time.

Though, the next rate of interest can have an antagonistic impact on funding methods targeted on development shares, as many businesses – particularly within the know-how sector – have traditionally fuelled their development by the usage of low-cost debt. The greater cost of borrowing could make this tougher.

However, an funding portfolio that’s invested throughout the whole world inventory market is more likely to be influenced extra closely by the American central financial institution’s choices quite than these made on Threadneedle Street. Even the businesses that make up the FTSE 100, London’s benchmark index, derive most of their revenues from abroad.

The US Federal Reserve has not too long ago modified its rhetoric from “higher for longer” interest rates, to accepting that they have now “peaked”. Market-watchers now count on that the Fed may begin to lower rates of interest earlier than the autumn, but others don’t anticipate cuts till 2025.

The Fed opted final week to carry rates of interest regular for a sixth assembly in a row at their 23-year highs of 5.25pc to five.5pc.

Chairman Jerome Powell had warned that it’s nonetheless too early to declare victory towards cussed inflation after “a lack of further progress” in a blow to hopes of imminent charge cuts.

Meanwhile, the European Central Bank has already signalled it can scale back borrowing prices on June 6.

Laith Khalaf, of AJ Bell, stated: “There’s a great deal of speculation as to which of the big three western central banks is going to blink first and cut interest rates.”

{kind=link}