Spring actual property season begins early as homebuyers look to reap the benefits of decrease costs

Article content material

Article content material

January is normally a reasonably quiet month for homebuying. Not so this yr as gross sales have surged nicely forward of the spring home searching season.

One Bay Street economist, bemused by the early exercise, took a stab at determining why that’s occurring. What Bank of Nova Scotia‘s Farah Omran came up with is that potential homebuyers are trying to take advantage of still-falling home prices, while at the same time choosing variable-rate mortgages on the assumption that the “short-term pain” of higher rates will be worth it for the “long-term” gain of lower rates when the Bank of Canada finally makes its cuts.

Advertisement 2

Article content

“The housing market has seen a surge in sales in recent months, even though the Bank of Canada has not yet started cutting its policy rate or even signalled that a cut is imminent as many have been expecting,” she said in a note on Feb. 14. “This surge in activity is sooner than we expected, particularly as it well precedes the spring season, which is typically a hot season for the housing market.”

Canadian home sales rose 22 per cent in January, signalling a possible “turnaround” in the sector, according to the Canadian Real Estate Association (CREA). The jump came on the heels of an 8.7 per cent increase in December. Despite the increase in activity, national benchmark prices in January fell 1.2 per cent from the month before, with CREA noting that prices continued to drop in areas where sales rose the most.

Omran said she believes more Canadians are taking out variable-rate mortgages and swallowing higher interest rates in the early going on the assumption that the Bank of Canada will cut rates later this year. Variable rates rise and fall with the prime rate, which is based on the central bank’s benchmark in a single day lending price.

Posthaste

Article content material

Advertisement 3

Article content material

Variable-rate mortgages, at the moment sitting at roughly seven per cent, had been out of favour. During the five-year interval from January 2018 to December 2023, new originations for variable-rate mortgages slumped to a low of 4.6 per cent in July 2023. The image has drastically modified. In December 2023, such mortgages accounted for 20 per cent of recent originations, based on Scotiabank.

“Buyers are pricing in a sure increase in house prices once cuts begin and are therefore choosing variable mortgages now, betting that the cuts will be significant enough to offset the higher initial payments and reduce the overall cost of the mortgage over the long term,” Omran mentioned.

The second a part of her idea has to do with the value of housing. She mentioned homebuyers are leaping on decrease costs now on the expectation that costs will rise as extra folks flood into the market as soon as rates of interest begin to drop.

Certainly, previous shopper behaviour has borne that out.

The housing market took off when Bank of Canada governor Tiff Macklem signalled a “conditional pause” in rate of interest hikes in early 2023. From February to early June, when Macklem restarted his mountaineering marketing campaign, the common nationwide home worth rose 10 per cent, based on CREA information, as folks rushed to reap the benefits of decrease mortgage charges.

Advertisement 4

Article content material

“Given the widespread expectation, of everyone from the BoC to CREA to most economics shops, that rate cuts will eventually lead to an uptick in activity and prices, this is a reasonable bet on the part of buyers,” Omran mentioned.

Of course, price cuts are the important thing, however stronger-than-expected inflation and jobs information have compelled economists to revise their expectations of when they are going to occur.

Some had referred to as for the primary price reduce to return in April, which might begin undoing the cycle of 10 will increase that lifted charges to 5 per cent. Now, many economists forecast a primary reduce in both June or July. Scotiabank, a little bit of an outlier, is looking for the primary reduce late within the third quarter, Omran mentioned in an e mail, and 75 foundation factors of cuts in contrast with the financial institution’s preliminary name for cuts totalling 100 foundation factors beginning within the second quarter.

“However, what seems to have brought this process forward is buyers’ willingness to put up with some short-term pain for long-term gain,” she mentioned.

Posthaste is taking a break Monday for Family Day. We’ll be again in your inbox on Tuesday, Feb. 20.

Advertisement 5

Article content material

Sign up here to get Posthaste delivered straight to your inbox.

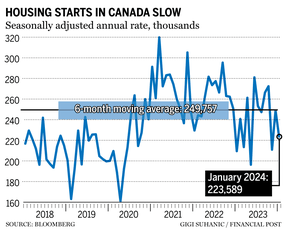

The national housing agency says the seasonally adjusted annual rate of housing starts came it at 223,589 units for the first month of the year compared with 248,968 for December 2023.

The decrease came as the annual pace of urban housing starts fell 11 per cent to 208,119 units, with the pace of multi-unit urban starts down 14 per cent at 164,789 units and single-detached urban starts up 0.08 per cent at 43,330 units.

The annual rate of housing starts in Toronto were up 179 per cent, boosted by an increase in multi-unit starts; however, Montreal fell 28 per cent and Vancouver dropped 55 per cent due to drops in multi-unit starts.

The annual rate of rural starts was estimated at 15,470.

The six-month moving average of the monthly seasonally adjusted annual rates of housing starts in January was 244,827, down two per cent from 249,757 units in December 2023.

— The Canadian Press

- Commissioner of Competition v. Cineplex Inc. listening to earlier than the Competition Tribunal relating to the competitors bureau’s misleading advertising practices case in opposition to the theatre chain.

- Canadian Radio-television and Telecommunications Commission hosts a five-day listening to for its evaluate of the wholesale high-speed web access framework

- Today’s information: Statistics Canada releases information on wholesale gross sales and worldwide securities transactions for December; U.S. Census Bureau releases information for housing begins and building permits for January.

- Earnings: Air Canada, TC Energy Corp.

Advertisement 6

Article content material

Get all of right now’s high breaking tales as they occur with the Financial Post’s reside information weblog, highlighting the business headlines it’s essential know at a look.

Recommended from Editorial

Relying on the Canada Revenue Agency’s Auto-fill may be expensive as this tax case over lacking earnings reveals. Read tax professional Jamie Golobek’s column right here.

***

Are you frightened about having sufficient for retirement? Do it’s essential modify your portfolio? Are you questioning methods to make ends meet? Drop us a line at [email protected] together with your contact data and the overall gist of your downside and we’ll attempt to discover some specialists that can assist you out whereas writing a Family Finance story about it (we’ll preserve your identify out of it, after all). If you have got a less complicated query, the crack staff at FP Answers led by Julie Cazzin or one among our columnists may give it a shot.

Advertisement 7

Article content material

McLister on mortgages

Flummoxed by the mortgage market? Robert McLister is right here to assist. Today, the Financial Post is launching a brand new column by the mortgage strategist that may assist our readers navigate the complicated sector, from the latest developments to complicated financing alternatives they gained’t wish to miss. To kick it off, Rob runs down the ten issues he’ll be watching most intently this yr, from the rate-cut ready recreation to the rise of the six-month mortgage and extra.

Read it right here

Today’s Posthaste was written by Gigi Suhanic, with further reporting from Financial Post employees, The Canadian Press and Bloomberg.

Have a narrative concept, pitch, embargoed report, or a suggestion for this text? Email us at [email protected].

Bookmark our web site and help our journalism: Don’t miss the business information it’s essential know — add financialpost.com to your bookmarks and join our newsletters right here.

Article content material

{kind=link}