Like a whole bunch of 1000’s of homebuyers within the UK yearly, Steve didn’t assume twice earlier than making use of for a short-term fixed-rate mortgage. It was solely when his software was rejected on a technicality that the Somerset-based IT skilled seemed for different choices.

A mortgage dealer steered he attempt a brand new lender referred to as Perenna. He was first impressed that the lender “applied a bit more common sense” to the technicality in regards to the phrases of the lease on his flat that had stymied his final software.

But he additionally learnt that the mortgage on provide was basically completely different. Perenna, which obtained a full banking licence final yr, affords a hard and fast rate of interest for the complete lifetime of its mortgages, as much as 40 years.

“It won’t go down, but it won’t go up,” says Steve, who selected a 25-year mortgage and who requested the FT to not use his actual identify. “Given the markets and everything at the moment, it’s nice to know . . . that it’s not going to change.”

Perenna is considered one of a handful of lenders now providing debtors the selection to repair their rate of interest for many years, in a bid to disrupt the £1.6tn UK mortgage market.

Rising mortgage charges have been the dominant characteristic of the property market prior to now two years, and a serious contributor to the UK’s cost of dwelling disaster.

Loans issued throughout the period of ultra-low rates of interest are actually reaching the tip of their phrases, with 1.6mn households as a consequence of see their mounted charges finish in 2024, in response to UK Finance.

A typical borrower who took out a two-year repair at 1.6 per cent in 2022 will face a 42 per cent improve of their month-to-month funds, in response to calculations by Zoopla, the property portal.

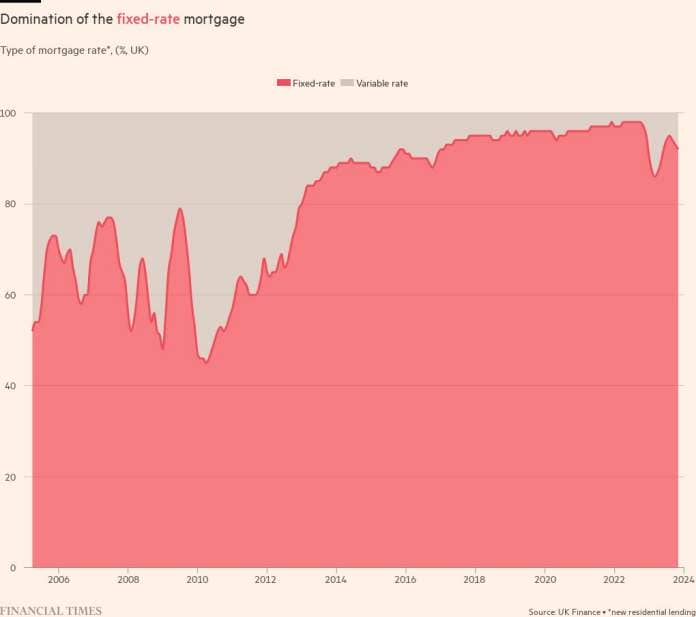

The sudden soar to a lot increased borrowing prices has highlighted an oddity of the UK mortgage market: the unusually excessive portion of short-term mounted loans. More than 90 per cent of UK debtors take out a fixed-rate mortgage for 5 years or much less.

Long-term fixed-rate mortgages are the norm within the US. Locking in for greater than 10 years is the commonest alternative for debtors within the Netherlands, Denmark and different European international locations.

Short-term charges are in style within the UK for his or her low preliminary cost and the flexibleness they permit for debtors who foresee themselves flipping their first home to maneuver up the property ladder. But the construction of the mortgage market has been blamed for making it tougher for first-time consumers to get on the housing ladder in any respect.

Short-term offers additionally power people to second-guess the rate of interest cycle, a problem that often wrongfoots economists {and professional} merchants, leaving them uncovered to rate of interest shocks.

“Nobody talks about the elephant in the room. Our mortgage market is not fit for purpose,” says Perenna founder and chief govt Arjan Verbeek. “All the European peer countries have better functioning mortgage markets . . . People are protected from a mortgage rate shock.”

Verbeek’s argument has gained traction with politicians. Shadow chancellor Rachel Reeves has hailed the potential advantages of long-term fixes to assist a “revolution” in home possession.

She has mentioned long-term offers might make sense “for a lot of people, especially for families” as a result of “potentially you would be able to borrow a bit more, to put down a bit less of a deposit. If you can take out some of that stress and instability, that will make a difference”.

Labour has pledged to review different international locations the place these loans are extra frequent, and work with lenders to “encourage increased offering of longer-term fixed-rate mortgages”.

Home possession charges in England have stagnated for a decade, after falling from their peak earlier than the 2008 monetary disaster.

The housing market has turn out to be more and more divided between households who personal their houses, and can assist their kids on to the property ladder and people with out fairness who’re being left behind. The variety of owner-occupiers with a mortgage has fallen by 2mn since 2002 and sits at ranges final seen within the Eighties, in response to Building Society Association analysis.

Higher home costs and tighter lending standards imply that the common first-time purchaser deposit has risen from £22,600 to £68,700 over 20 years, rising from 0.6 instances common incomes to 1.2 instances, in response to CBRE.

“There are good reasons for any government at any time to want a nation of homeowners,” says Yolande Barnes, chair of the Bartlett Real Estate Institute at UCL. “From a practical point of view, the last thing you want is a whole load of millennials retiring with no equity.”

But the thought additionally faces scepticism. Many lenders say there’s little demand from customers and that nurturing that demand shall be a serious problem, on condition that these product are unfamiliar and dearer upfront. Regulatory reform can be more practical in serving to consumers, they argue.

“It always, invariably, looks much cheaper to get the two- and five-year fixed rate,” says Simon Gammon, a dealer at Knight Frank Finance. “The peace of mind of a longer term mortgage doesn’t look worth it compared to the rate.”

Ian Mulheirn, a researcher on the Resolution Foundation, says the “obsession” with building extra houses has obscured the very important significance of access to credit score for aspirant consumers.

“The question is: who bears the risk?” says Mulheirn. “We have been in this market where we just say households bear the risk of interest rates going up, of losing their jobs, of house prices going down.

“The big picture story is: is it sensible to leave these risks on households’ shoulders and try to regulate to protect them, or is there a better way of doing this whole thing?”

The home mortgage is one of the vital commonplace types of debt on the earth, however the monetary structure behind these loans differs considerably from nation to nation.

In the UK, home loans are funded partially from deposits and lenders carry the chance of default. Insurance to guard towards defaults, widespread within the Nineties, is now not often used.

“If [longer-term fixed rates] do take off and proliferate, the banks and building societies will have to look at their funding model in the future and what that means for them because they don’t have those long-term savings that they can rely on for 15, 20, 25 years,” says Charles Roe, mortgage director at commerce physique UK Finance.

Mortgage pricing is predicated on the cost of “swaps”, by-product contracts that banks use to handle their rate of interest danger. In concept, debtors profit from a less expensive mounted charge for 2 or 5 years, after which roll on to a better “standard variable rate”, presently round 8.5 per cent on common. In actuality, most debtors refinance on the finish of the mounted charge and by no means pay the upper variable charge.

Regulations designed to guard the monetary system after the 2008 monetary disaster require banks to “stress test” mortgage candidates, typically to no less than 1 per cent above the present customary variable charge.

That means somebody shopping for an averagely priced home on a five-year repair at 4.84 per cent and presently paying round £1,300 per thirty days could be stress examined to ensure they’ll afford a 9.5 per cent rate of interest and month-to-month funds of near £2,000.

Stress assessments create a entice for prosperous renters. Some households pays extra in hire than they might pay for his or her mortgage, however can’t qualify for a mortgage as a result of they fail the stress check. Older candidates are additionally barred if the mortgage time period stretches into retirement.

The concept of reforming the UK market with longer-term charges was included in Boris Johnson’s 2019 election manifesto, and analysed in a government-commissioned research as way back as 2004.

But the launch of Perenna provides these coverage concepts a practical and entrepreneurial champion. For the start-up financial institution, the stress check is mainly irrelevant as a result of the month-to-month funds by no means change.

The firm says it is going to lend as much as six instances the borrower’s revenue, far increased than the usual 4.5 instances from excessive road banks. And it could actually lend to retirees supplied the repayments are reasonably priced on their mounted revenue.

The rates of interest on its loans are between 0.12 and 0.89 proportion factors greater than the brief, mounted offers, relying on the tenure and deposit. But for a pair with a joint revenue of £60,000, Perenna says it might provide a most mortgage of £307,489, giving the customer an additional £72,000 in contrast with a mortgage on customary phrases.

Perenna borrowed concepts from Denmark, Germany and Verbeek’s native Netherlands to design its new product. The former credit standing analyst and his workforce have labored since 2018, funded by enterprise capital agency Silverstream, to arrange the corporate and acquire a banking licence.

Perenna doesn’t take deposits, however as a substitute plans to fund mortgages by packaging them into bonds that may be offered to traders. It plans to promote the primary bonds this yr as soon as it has sufficient mortgages on its books.

Borrowers face the identical early compensation prices as a traditional five-year repair, Perenna says. After 5 years there isn’t any penalty for repaying the mortgage early or refinancing at a greater charge. Mortgages are additionally transportable, topic to situations, if the borrower strikes.

Verbeek says there’s vital demand for mortgage-backed bonds from pension suppliers, who must match their obligations to retirees towards dependable long-term revenue streams.

“There is nothing more natural than the young family paying £500 to pay off their mortgage and that money going to the pensioner next door,” he says. “We take domestic savings and put them into the domestic economy.”

But pension managers sometimes need long-term and assured revenue to fund payouts to retirees, so Perenna should fastidiously handle the phrases of its bond issuance to steadiness assembly traders’ calls for and providing flexibility to debtors.

Advocates imagine that if lenders can discover a solution to navigate these challenges it might unlock home possession for a brand new cohort of first-time consumers. A 2019 Centre for Policy Studies paper estimated a further 1.9mn renters might access a long-term mortgage.

Other reforms might additionally play a task. A research by the Tony Blair Institute discovered that debtors with a smaller deposit and due to this fact a better loan-to-value (LTV) ratio are charged a larger rate of interest premium within the UK.

In different international locations, mortgage insurance coverage mitigates the chance premium for top LTV loans. Even after paying for insurance coverage towards default, consumers can nonetheless save money. In Canada and Australia, such cowl is usually obligatory for low-deposit loans.

In a report printed yesterday, the Building Society Association urged different coverage adjustments to redress the steadiness between guaranteeing monetary stability and permitting access to credit score. It mentioned long-term fixes “offer a number of attractions” however had but to entice many debtors.

Other consultants, similar to Barnes at UCL, imagine the issue comes right down to basic financial situations. She argues that within the twentieth century, mortgages had been profitable in “transferring an enormous amount of equity from landlords to their former tenants”. Consistently increased inflation rapidly eroded the real-terms worth of these loans, making them extra reasonably priced.

“We’re in a different era that does not favour debt in relation to real estate purchases,” she says. Policymakers ought to concentrate on different options, similar to methods for tenants to step by step purchase fairness off their landlords, she provides.

“The danger of trying to copy 20th century models from other countries is that you’re missing what the actual problem is.”

The extra rapid problem is convincing customers to attempt longer-term loans.

Few lenders presently present multi-decade fixes. Specialist lender Kensington affords mounted charges for as much as 40 years whereas April Mortgages, a wing of Dutch asset supervisor DMFCO, has merchandise as much as 15 years within the UK market.

If longer fixed-rates caught on they may considerably disrupt the UK mortgage sector. Critics of the present construction argue that banks rely on a sure proportion of debtors falling off the carousel of mounted charges and paying the costly customary variable charge for a time period. UK Finance says round 7 per cent of debtors are on SVRs at anybody time, though typically it is because they’re anticipating to promote their home within the close to future.

Mortgage brokers, who present fee-based recommendation to debtors, additionally depend on the regular churn of brief fixes coming to an finish. “There’s a whole economy based on reviewing your rate every two and five years,” says Knight Frank’s Gammon.

But short-term offers additionally provide a less expensive rate of interest up entrance. And many UK debtors need the flexibleness transfer up the housing ladder.

“In the UK, we do have an aversion to fixing for that length of time,” says Roe. “Most people’s marriages don’t last 25 years so, you know, fixing your mortgage for 25 is pretty hopeful.”

Banks already providing seven and 10-year fixes have seen very low take-up from clients, say business representatives. Liam O’Hara, head of mortgages at HSBC, says that the UK has developed a “highly dynamic” market the place lenders compete laborious to supply the most affordable short-term charges.

Expectations that the Bank of England will quickly minimize charges is additional damping demand for long term merchandise, he provides.

Ryan Etchells, chief business officer at Together, a specialist mortgage supplier that is likely one of the UK’s largest non-bank lenders, says short-term fixes fitted a sample of home possession within the UK the place consumers flip properties extra rapidly.

“The traditional UK trend in home buying is that customers move up the ladder over the course of their lives. The European trend is that people live in their homes for longer. We’re starting to see the European trend come into the UK market,” he says.

But after a recent market research, Together determined to not launch a long-term mounted product. “If we brought that product to market, we don’t think it would be meeting enough customers’ needs to make it attractive, frankly,” says Etchells. “The market demand just isn’t there yet.”

{kind=link}