Families are getting slammed by their mortgages. Anyone who purchased a home in 2020 loved a few years the place their home worth went up whereas they paid rates of interest that had been roughly zero.

But then the Reserve Bank of Australia (RBA) determined the nice instances had rolled too lengthy. The central financial institution fetched a long-forgotten trick from the again of the cabinet: the speed hike.

They dusted it off and put it to work, piling on the ache. Official rates of interest rose from mainly zero to 4 per cent, whereas mortgage charges rose from round 2 per cent to over 5 per cent.

That added $1000 a month to mortgage repayments on the typical new home mortgage in New South Wales.

Who has a spare $1000 a month? Not everyone, that’s for positive. There’s been a world of harm for households as they tackle extra shifts at work and lower bills so that they’re not spending greater than they make every month.

RELATED

The ones most within the crosshairs are the young households.

Those with new home loans and little youngsters. They’re experiencing a cost-of-living rise of greater than double inflation just lately: 6 per cent.

But they don’t have a number of fairness of their properties, nor have they got offset accounts full of further home mortgage repayments.

The whinging, nonetheless, comes from a wider cross-section than simply young homebuyers.

And if we take a look at the info we discover that a few of these individuals don’t have fairly a lot to complain about.

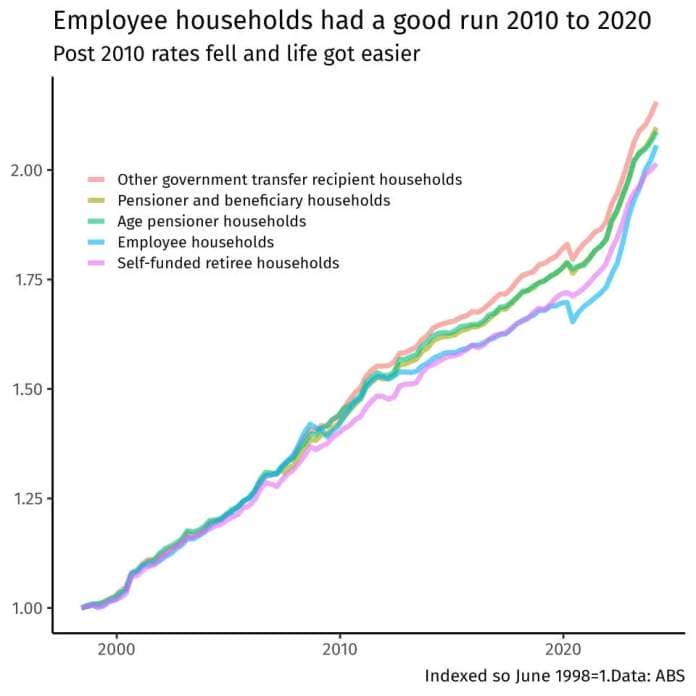

The Australian Bureau of Statistics published cost-of-living indexes for a variety of teams in society so we are able to see how the final price of inflation impacts totally different households in another way.

What it reveals is that the cost of residing for “employee households” has been rising extraordinarily sharply just lately. But that comes after a really lengthy interval the place life received a little bit cruisy.

The subsequent chart reveals the cost of residing index, the place all totally different households re set equal again in 1998, so we are able to simply evaluate adjustments since.

It reveals life has received steadily more durable for pensioner and beneficiary households.

But worker households who already had mortgages had been taking part in on straightforward mode for a lot of the interval between 2010 and 2020.

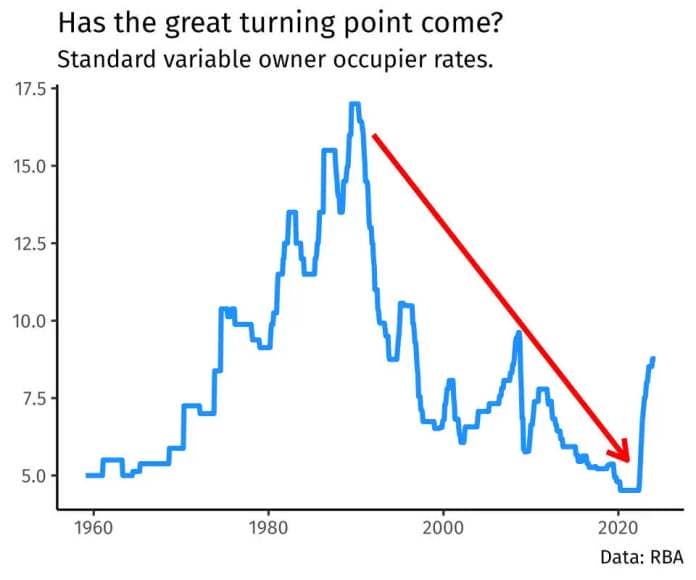

From mainly the Nineteen Nineties to now, mortgage charges have been falling for more often than not.

And particularly from 2010 to 2020, as the following chart reveals.

The large query is whether or not our present second is a bit like 1970 and charges are going to surge additional upwards from right here.

If so, the ache being dished out to young mortgage holders is way from over.

{kind=link}