Kerkez

It’s had to do with 5 ½ months because I composed my “prevent the stock however offer the put” post on PetMedication Express, Inc. (NASDAQ:ANIMALS) stock, and because time the shares have actually returned a loss of 8.3% versus a loss of 2.4% for the S&P 500. The business has actually simply reported financials, and market appears to disapprove, considered that the stock is down 5.2% today. I wish to examine these financials since a stock because, and I wish to examine those. Additionally, a stock trading at $19.40 is, by meaning, a less dangerous financial investment than one that’s trading at $21.40. I’ll choose whether to purchase the stock by taking a look at these monetary outcomes and comparing them to the evaluation here. Also, the puts that I advised because post have actually simply ended useless, which was pleasing enough, however it implies that I require to do some more work and attempt to comprehend whether it makes good sense to lastly purchase the stock, compose more puts, or remain on the sidelines.

Welcome to the common “thesis declaration” part of the post, dear readers. It’s here where I provide you the highlights of my thinking so that you will not require to check out all 1,900 words unless you truly wish to do that to yourself. You’re welcome. Although I’m enthusiastic for the future, the monetary outcomes have actually been average in my view. They’re not as bad as they remained in the second quarter in my view, however they were bothered. As an outcome, the evaluation is much more extended, and the dividend yield is even lower. For that factor, I’ll stay on the sidelines. That composed, I will be offering places on this name today as the premia available is rather great for deep out of the money puts in my view. This trade exercised well in the past. I made $.75 selling puts, and I choose that result to what might have been a $2 per share loss. Today I’ll be offering the very same strike for about $.80.

Financial Snapshot

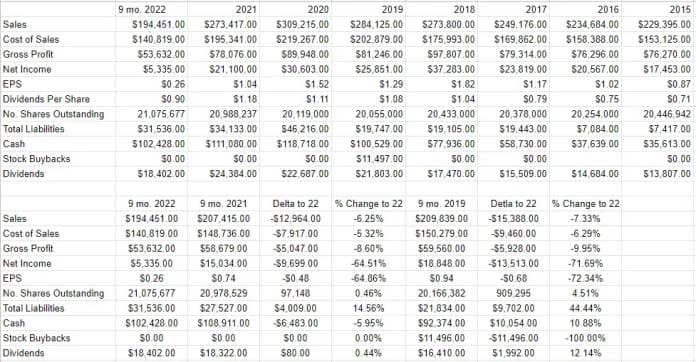

I’d state the most current monetary outcomes were not excellent. Compared to the very same duration in 2021, the very first 9 months of 2022 have actually been rather soft. Revenue was down by about 6.25%, and gross earnings was down by about 8.6%. Results were lower when compared to the very same duration in 2019, with income and gross earnings in 2022 off by 7.33%, and 9.95%, respectively. That’s bad, however it truly gets bad when you compare earnings throughout the most current duration to the very same time in 2021. In spite of a downturn in income, the business increased G&A expenses by $7.9 million, or 35.4%. That was a substantial driver in the $9.7 million decrease in earnings from in 2015 to this. The very same photo emerges when we compare the most current outcomes to the pre-pandemic period. Net earnings in 2022 had to do with 72% lower than it remained in 2019.

At the very same time, the capital structure has actually weakened rather. I’m less worried about this, since it is still really strong, however I remain in the state of mind to note it, so I will note it. Total liabilities have actually approached by $4 million, or 14.5%. Admittedly, the business still has money on the balance sheet that represents over 3.25 times overall liabilities, however the pattern has actually not been excellent in my evaluation.

Given the massive money stockpile, I have actually not altered the view revealed in my earlier post that the dividend is well covered here. It has actually grown well over the previous 12 ½ years, and, provided the money stockpile, I do not believe there’s threat of a cut here anytime quickly. Additionally, the business does contend in a colossus of a market, so I believe there is chance for them to start to grow once again. I believe is specifically the case provided the just recently revealed acquisition of PetCareRx. Given the above, I’d be really happy to purchase the best cost.

PetMedication Financials (PetMed financier relations)

The Stock

If you read my things routinely you understand what time it is. It’s the time where I become a little bit of a monetary “shopping center police,” where I advise everybody that a business stands out from its stock. The business offers Pet medications at a revenue. The stock, on the other hand, is a notepad that gets traded around in a public market and is affected by an excellent numerous aspects, a lot of which are just peripherally associated to the underlying business. While the stock cost has actually been really adversely affected by the other day’s monetary outcomes, it’s likewise affected by the crowd’s ever-changing views about the business’s future monetary efficiency. Someone might stress, for example, about the possibility of a slowing dividend, which might affect the cost of the stock rather substantially. The stock cost likewise is possibly affected by the crowd’s ever-changing point of views on the relative benefits of “stocks” as a possession class. To usage PetMed as an example, some part of the loss seen because I last evaluated the name might be a function of the truth that the S&P 500 itself is down because. Admittedly, this is a counterfactual argument, however I believe an affordable case might be made to recommend that when the marketplace turns sour on stocks, individuals toss out monetary children with the indices bathwater. While this is tedious, it’s possibly successful. If we can find the inconsistencies in between the crowd’s take on a provided business, and the presumptions embedded in the cost, we can make a revenue.

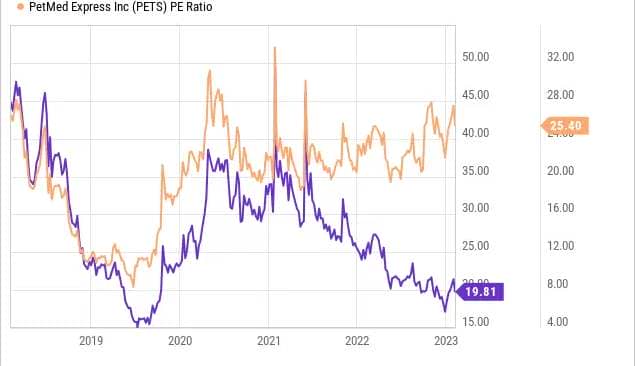

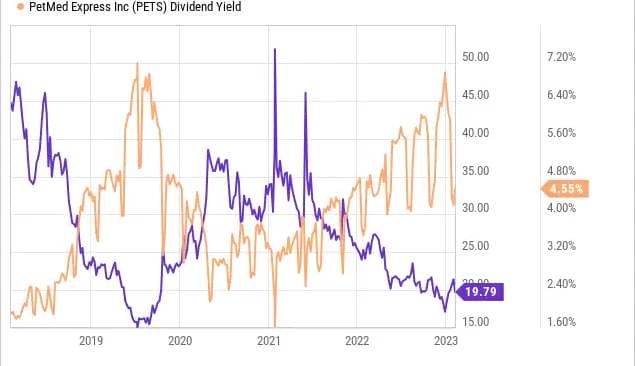

Finally, I must mention that I’ve discovered that less expensive stocks use a greater risk-adjusted return, so I like to purchase shares when I consider them to be low-cost and avoid them when they get costly. If you are among my routine readers you understand that I determine the cheapness (or not) of a stock in a couple of methods, varying from the basic to the more intricate. On the basic side, I take a look at the ratio of cost to some procedure of financial worth like sales, profits, complimentary capital, and so on. Ideally, I wish to see a stock trading at a discount rate to both its own history and the general market. In my previous missive on PetMedication, I defined my handle their evaluation onomatopoeically as “meh.” For example, the shares were trading at a cost to profits ratio of about 22, and the dividend yield was 5.65% at the time. The shares are now about 15% more costly as an outcome of the drop in cost, and the dividend yield has to do with 19.5% lower, per the following:

I should inform you, dear readers, that I do not love the concept of paying more and getting less.

My regulars understand that I believe ratios can be explanatory, however I likewise wish to attempt to exercise what the marketplace is “believing” about a provided financial investment. If you read my things routinely, you understand that the method I do this is by relying on the work of Professor Stephen Penman and his book “Accounting for Value.” In this book, Penman strolls financiers through how they can use some quite basic mathematics to a basic financing formula in order to exercise what the marketplace is “believing” about a provided business’s future development. This includes separating the “g” (development) variable in this formula. In case you discover Penman’s composing a bit nontransparent, you may wish to attempt “Expectations Investing” by Mauboussin and Rappaport. These 2 have actually likewise presented the concept of utilizing the stock cost itself as a source of details, and we can presume what the marketplace is presently “anticipating” about the future. Applying this technique to PetMed at the minute recommends the marketplace is presuming that this business will grow profits at a rate of ~8% in eternity. I think about that to be an extremely positive projection for any business, even one with a current development profile like this.

Given all of the above, I’m going to continue to prevent this name. The shares are less expensive in cost now, however the truth is that the business appears to have some obstacles growing. I wish to see some proof of continuous success prior to purchasing strongly.

Options As Alternative

In my previous missive on this name, I advise shunning the shares similar to I am today, however I was comfy owning the stock at the best cost. Specifically, I was, and am, comfy owning this stock at $15 per share, so I offered 10 of the January 2023 puts with a strike of $15 for $.75 each. I like this sort of trade since it is a “win-win” in my evaluation. If the shares crashed listed below $15 from $22, I’d be the happy owner of a fairly good business at an excellent cost. Since the shares stayed above $15, I merely gathered the premia which likewise was not a challenge.

I like to attempt to duplicate success when I can, and because of that, I’ll be offering puts once again today. Specifically, I like the September PetMedication puts with a strike of $15, which are presently bid at $.80. So, one of 2 things can take place over the next 8 months. Either the shares will be “put” to me at a net cost of $14.20, or I’ll gather much more choices premia. Note that holding all else consistent, if the shares are put to me, that would represent an effectively covered dividend yield of 8.45%. So, I’ll either make another $.80 per share, or I’ll lock in an extremely good dividend yield. This is why I consider this trade to be a “win-win.”

It’s time, as soon as again, to discuss threat. It’s all well and great for a complete stranger on the web to discuss “win-win” trades, however if you’re going to trade these, you require to be warned of the truth that this financial investment, like all financial investments, includes threat. I think about the threats connected with these instruments to fall under 2 broad classifications: the financial and the psychological.

Starting with the financial threats, I’d state that the brief puts I supporter are a little subset of the overall variety of put choices out there. I’m just ever going to offer places on business I’d want to purchase, and at costs I’d want to pay. So, I would never ever promote that individuals merely offer puts either “willy” or “nilly” with the greatest premia. In my view, that method would result in devastating outcomes. So my very first little bit of recommendations is to just ever offer places on business you wish to own at (strike) costs you’d want to pay. Take my word on this one, as it’s notified by agonizing history.

The 2 other threats connected with my brief puts method are both psychological in nature. The initially includes the psychological discomfort some individuals feel from losing out on advantage. To utilize this trade as an example, let’s presume that PetMed stock cost goes parabolic and strikes $50 per share in between now and the 3rd Friday of September. Obviously my puts will end useless, which is an excellent result in some methods. I will not capture any of the advantage in the stock cost, however. So, short put returns are capped by the premium received. This may be emotionally painful, but my attitude is that if the shares are a bit rich at $19, they’d likely be destined for a fall at $50, so no harm, no foul.

Secondly, it can be emotionally painful when the shares crash below your strike cost. So far, whenever this has happened to me, things have worked out well over the long term, because I insist on only ever writing puts at “screaming buy” strike prices. That said, it has been emotionally stressful in the brief term on occasion. If you’re going to sell puts, please be aware of this phenomenon.

If you understand these risks, and can tolerate them, I would recommend that you sell puts. For my part, I’m going to replace the puts that expired last month with this new crop of $15 strike costs. If you’re comfy with offering puts, I believe they use the very best threat adjusted returns at this moment.

{kind=link}