Vanessa Pham constantly has plenty to fret about as president of Omsom, a fast-growing Asian food set business. But the possibility of losing all her start-up’s money in a bank run was not one of them — previously.

On March 9, she discovered herself rushing to withdraw Omsom’s money from Silicon Valley Bank. Pham was at a huge food convention in Los Angeles when she began getting disconcerting messages from her financiers. The day in the past, SVB revealed it had actually offered a bond portfolio at a $1.8bn loss and was seeking to raise $2.25bn in brand-new equity to support its balance sheet. All of Omsom’s money remained in an SVB account that by the end of the day she might no longer gain access to.

Pham was simply among countless Americans captured up in the monetary panic of the previous month. The fast boost in rates of interest exposed fractures in how some banks have actually handled their balance sheets. Three lending institutions have actually collapsed, a 4th is still on the ropes. Billions have actually been rubbed out the marketplace assessment of banking stocks.

The crisis has huge ramifications for United States local banks and their financiers. Perceptions of threat have actually moved greatly. Tougher policy and lower success appear unavoidable. Beyond this, United States rate of interest policy might now follow a gentler, slower trajectory.

Such factors to consider were a million miles from Pham’s ideas as backers prompted her to get Omsom’s funds out of SVB. But it was far too late. Quicker consumers had actually started withdrawals for $42bn that day, leaving the bank with an unfavorable money balance of $958mn.

The next day, regulators actioned in and took control of SVB. It had actually taken less than 40 hours for a leading 20 bank with $209bn in overall properties to end up being the second-largest bank failure in American history after Washington Mutual in 2008.

“I never thought my money would be unsafe in a bank in the US,” Pham remembers.

Millions of Americans have had the very same wake-up call and are taking a tough take a look at where they keep their money. Two days after SVB’s collapse, New York-based Signature Bank folded after a comparable depositor run. First Republic Bank got an industry-led emergency situation money injection and has actually employed Lazard and JPMorgan Chase to recommend it on tactical alternatives. Pacific Western Bank needed to rely on financial investment company Atlas SP Partner for a $1.4bn funding center.

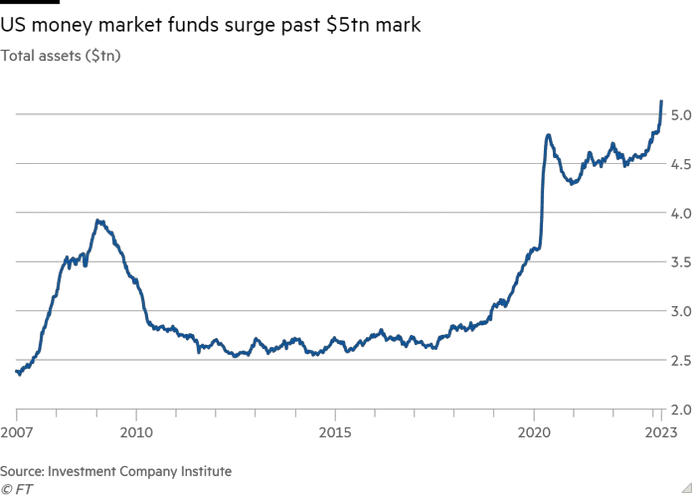

Policymakers have actually taken amazing actions to stop panic amongst depositors. Nonetheless, deposits at little banks visited $120bn, or about 2.2 percent, in the week to March 15, according to information from the Federal Reserve. Separate information reveals that almost $240bn has actually flooded into money market funds in the 2 weeks to March 22. Whether this deposit flight eases off or continues will play a huge function in identifying the health of the nation’s smaller sized banks and the businesses they serve.

The screen

The United States Federal Deposit Insurance Corporation covers more than 4,200 business banks, or one lending institution per 80,000 residents. By contrast, the UK just has 260 banks, or one bank for every single 257,000 individuals. In the United States, banks run the range — from top-tier Wall Street names such as JPMorgan to local powerhouses such as PNC and neighborhood banks with less than $100mn in properties. Smaller lending institutions typically service cities and specific niche markets underserved by bigger banks.

Financial panics are unforeseeable, sent by word of mouth and its contemporary equivalent, social networks. But the deposit flight has actually not been completely approximate. It has actually singled out lending institutions with 2 attributes. First, a high level of uninsured deposits, which in this context indicates more than $250,000 per depositor. Second, a big space in between the fair-market worth and balance-sheet worth of its properties. SVB was an outlier in both aspects.

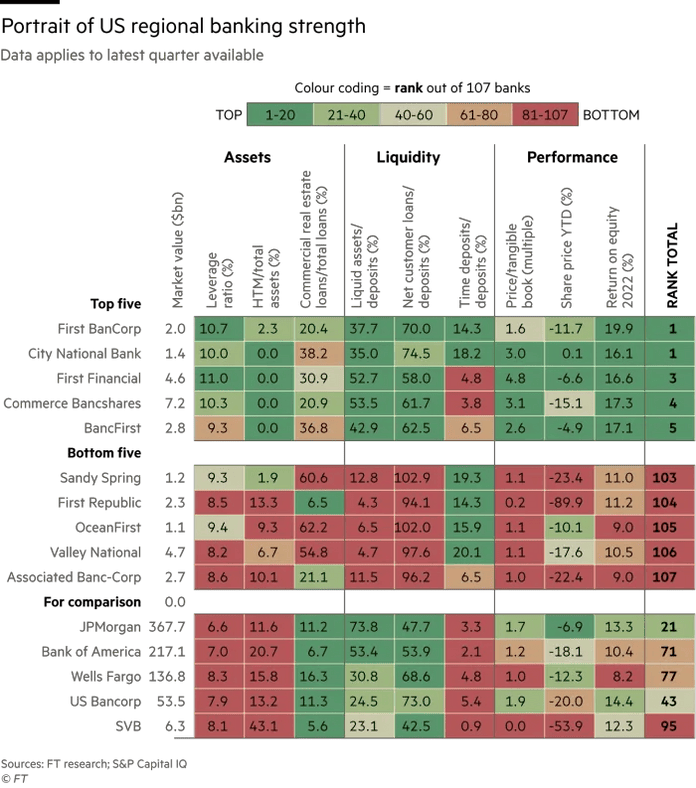

Lex has actually evaluated more than 150 United States banks to build a photo of the sector’s health. Like any other ranking, it is simply a photo of monetary metrics and there is no factor to believe that any of the smaller sized lending institutions on the resulting list that are trading usually will suffer an SVB-style collapse.

Financial panics are jointly unreasonable and might concentrate on attributes not vulnerable to screening. An example would be the extremely networked nature of SVB’s customer base in the west coast tech market.

Still, our screen discovered that extremely ranked banks usually had low levels of so-called hold-to-maturity securities, which can create heavy losses if they need to be offered in an emergency situation, and low direct exposure to business realty.

The greatest local banks in our screen were City National Bank of West Virginia, noted as City Holding Company, and FirstBank, which is priced quote as First RestrictionCorp and runs in the Caribbean and Florida.

Poorly-ranked banks undoubtedly had lower capital relative to their loaning and a lower ratio of liquid properties to deposits. The weakest gamers our screen determined were Wisconsin’s Associated Bank, noted as Associated Banc-Corp, and Valley National of New Jersey.

We ranked banks for 3 broad attributes: property durability, deposit liquidity and financier belief. Each of these containers included 3 procedures. These consisted of take advantage of ratio, liquid properties as a share of deposits and cost to concrete book worth respectively.

We limited our screening of S&P Capital IQ Pro information to noted banks with market capitalisations of more than $1bn to omit small lending institutions. We likewise neglected big financial investment banks, brokerages and banks with missing out on information. That left us with 107 organizations making up $14.6tn of properties of the United States banking market.

We have actually not changed rankings for the size of organizations above the $1bn market worth limit. That suggested market leviathan JPMorgan was available in a companionable joint 21st with FB Financial of Nashville. United States mega banks are unimpeachably safe or just too huge to stop working, depending upon your perspective. They are consisted of mainly for relative functions.

Future tense

Fed actions to supply liquidity buffers to banks ought to help avoid even more bank failures. In the meantime, depositor behaviour has actually altered. Banks will need to provide greater rates of interest to keep anxious consumers from defecting to competitors or putting their money into money market funds. That indicates financing expenses will increase, especially for smaller sized and midsized banks, and revenues will be squeezed.

“Profitability issues will apply to the whole banking sector, albeit in different magnitudes,” says Eric Compton, an equities strategist for Morningstar Research. “Big banks like Truist should see less funding outflow pressure and are likely to be receivers.” But others like First Republic threat ending up being so-called zombie banks unless they reorganize their balance sheet or draw back deposit streams.

Another concern: harder capital guidelines for midsize banks, presently under factor to consider from regulators, might even more restrict the market’s capability to extend credit to businesses. While the 25 most significant savings account for over 63 percent of the market’s overall properties, smaller sized savings account for 70 percent of business realty loans and 95 percent of loans protected by farmland.

Tighter loaning conditions might develop an unfavorable feedback loop that results in an economic downturn and more defaults. Commercial realty, already reeling from falling tenancy post-pandemic, is significantly viewed as the next pressure point on banks’ balance sheets.

“The liquidity crisis will pass,” says Thomas Simons, a money market economic expert at Jefferies. “But a credit crisis is coming.”

Nothing is truly run the risk of complimentary

Banks were flooded with almost $5tn of brand-new deposits throughout the pandemic. Armed with inexpensive money, numerous filled up on long-dated Treasuries or mortgage-backed securities that are ensured by the United States federal government. These used reasonably appealing returns when rates were low. American banks held $5.5tn of such securities on their balance sheets at the end of 2022 — a 44 percent boost compared to prior to the pandemic.

But the rates of these bonds fell when the Fed started to raise rates of interest strongly in 2015. Unrealised losses amounted to $620bn at the end of 2022, according to the FDIC.

Such paper losses just crystallise when a bank is required to offer these bonds and till they do, accounting guidelines permit them to soften the blow to capital adequacy. Security holdings can be categorized as “held-to-maturity” or “available-for-sale”. Any losses in the AFS basket need to be marked to market and deducted from the bank’s capital base, however those in the HTM basket are left out. To keep capital ratio steady, numerous banks have actually moved properties far from AFS towards HTM.

Proponents state HTM accounting assists banks limitation volatility in their equity and capital ratios. That can make good sense — as long as depositors don’t request their money back and banks can hold the bonds to maturity. Otherwise, HTM accounting can provide an incorrect sense of capital cushion.

That held true at SVB, whose $15.1bn of HTM losses were only simply covered by $16bn of equity at the end of in 2015. Its poor threat management was intensified by a focused customer base controlled by equity capital and tech start-ups. Some 94 percent of SVB’s deposits were uninsured and for this reason most likely to get away at the very first indication of problem, one of the most of any bank with more than $50bn in properties. As rates of interest increased, equity capital started drying up, requiring early-stage business to draw down funds hung on deposit at SVB to fulfill payrolls and other daily expenditures. Once SVB might not fulfill those withdrawals, it needed to start selling its securities portfolio at a loss.

“SVB woke people up to duration risk,” says Nathan Stovall, head of banks research study at S&P Global Market Intelligence.

A bank run for the digital age

The work on SVB was worsened by herd mindset and innovation. Fear and panic can rapidly spread out through social networks or WhatsApp groups. Rather than forming lines outside banks, depositors can take out funds with a couple of taps on their banking apps.

Systemic threat simply based upon size of the organization needs a rethink, according to Michael Held, partner at WilmerHale and formerly basic counsel at the New York Fed. “Clearly here it wasn’t size, it was herd behaviour, cascading run risk,” Held says.

This raises a thornier concern: can behavioural psychology be tension checked? Having taken deposit stability for approved throughout the years of low rates of interest, the marketplace now needs to find out how to design the probability of a bank run. No one best metric exists for this. But core deposits — money put by smaller sized depositors who usually live within the bank’s market location — is one proxy.

These are normally viewed as less vulnerable to changing than big accounts, which typically move amongst banks as rates of interest alter. For this factor, the Lex screen utilizes another metric — the level of time deposits that have a set duration prior to they can be withdrawn by consumers.

The other assessment space

First Republic’s HTM losses were no place as high as SVB’s. It reported a paper loss of about $4.8bn versus $17bn of investors equity at the end of in 2015. Instead, it is the assessment space in its loan book that has actually brought in attention.

For years, First Republic tempted high net worth consumers with cut cost rates on home loans and loans. A loan-to-deposit ratio of 94 percent recommends the San Francisco-based bank is utilizing almost all its deposits to money its loaning activities. It had $102bn worth of domestic realty loans on its books at the end of in 2015, almost all of which grow in 15 years or later on.

Higher yields on ultra-safe Treasuries have actually made these long-dated, jumbo home home loans look less appealing. The $19.3bn space in between the reasonable worth of its realty protected home loans and their balance sheet worth recommends as much. At the very same time, the deposits of its rich consumers are typically too huge to be guaranteed by FDIC — implying they are less sticky in times of tension. Unsurprisingly, First Republic’s stock cost is a fifth of its concrete book worth per share.

Where were the regulators?

Could recent occasions have been avoided? Even as the Federal Reserve has actually tightened its oversight of huge Wall Street banks in the wake of the 2008 monetary crisis, the reverse has actually been taking place for smaller sized organizations. The 2018 rollback of the Dodd-Frank act, the most significant deregulatory effort considering that the 2007-08 monetary crisis, raised the limit for banks to be thought about systemically essential to $250bn in properties from $50bn.

This mean banks with properties of approximately $250bn were excused from the Fed’s hardest supervisory procedures, consisting of tension tests along with capital and liquidity requirements.

“I think if we didn’t roll back Dodd-Frank in 2018, it would have been less likely that SVB’s problems went unnoticed,” says Saule Omarova, a teacher of law at Cornell University who was likewise as soon as President Joe Biden’s candidate to function as a leading banking regulator. “SVB would have been subjected to additional requirements — like liquidity coverage ratio and net stable funding ratio — which is also important as a procedural matter. If you have to undergo stress tests several times a year, you would need to establish better internal controls. You would have an incentive to rebalance your portfolio more nimbly.”

The banks evaluated by Lex usually hold liquid properties equivalent to about a quarter of deposits. This is an easier procedure of liquidity than LCR, which determines liquidity relative to short-term commitments. JPMorgan is near the top of our ranking at almost three-quarters. Second from bottom, First Republic held liquid properties equivalent to simply 4 percent of deposits.

Profits: lower for longer?

A barrage of federal government actions — consisting of the production of a brand-new emergency situation loaning center — are assisting stop short-term liquidity concerns by providing banks access to adequate financing to pay to depositors.

But these funds do not come inexpensive. The Fed’s Bank Term Funding Program — where banks can promise their security holdings as security for loans — charges the 1 year over night index swap rate (presently at about 4.68 percent) plus 10 basis points, for making use of the center. Loans from the Federal Home Loan Bank system, considered as the lending institution of second-to-last resort, charges likewise raised market rates.

Depending on the length of time banks need to obtain at these rates and just how much they make from the properties on their books, net interest earnings will come under pressure. As an outcome, the Fed might decide to raise rates more gradually with the objective of decreasing additional shocks to the monetary system.

Ultimately, banks will require to recover deposits, which are the most affordable form of financing. This is no simple task provided the greater rates available somewhere else and shaken self-confidence in United States banks.

Pham, as president of a start-up, is illustrative of this shift. She ultimately restored access to her business’s funds held at SVB. But she now divides the money in between 3 various banks and is checking out utilizing various kinds of accounts — consisting of those that would sweep her money into money market funds.

“Watching a trusted system fail us has made me more thoughtful about where we store our funds,” she says.

Data visualisation by Chris Campbell

{kind=link}