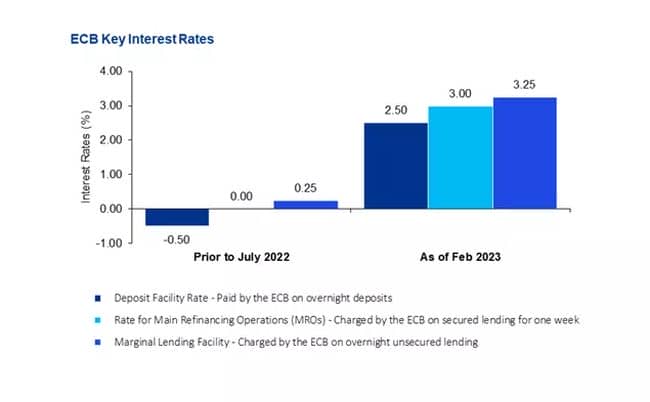

ECB Interest Rates

In January 2023, customer inflation in the Euro location stood at

8.6%1. In Malta, the yearly inflation rate stood at

6.8%2. If it weren’t for Government’s choice

to keep energy rates repaired, this would usually be greater.

The European Central Bank (ECB) targets an inflation rate of

2.0% over the medium term to satisfy its main function of

preserving cost stability throughout the Euro location. It was for that reason

not a surprise when the ECB chose to increase rate of interest and

reverse a years long pattern of low or unfavorable interest rates.

Source: ECB information; KPMG analysis

How does increasing rate of interest reduce inflation?

The present aspects increasing inflation internationally are the

remaining effect of the pandemic on supply chains, and the continuous

war in Ukraine, which affected the supply of oil, gas, and grains,

explaining the especially high rates of energy and food

inflation.

When rate of interest increase, the greater cost of obtaining

dissuades customers from purchasing products typically gotten through

bank financing, such as property, vehicles, and equipment. Higher

obtaining expenses likewise leave less money left over to invest in

daily products such as clothes, taking a trip, and eating in restaurants. In

turn this reduces the aggregate need for items and services,

eliminating inflationary pressures. Higher rate of interest likewise

motivate more conserving and subsequently less spending.

Loan and deposit rate of interest in Malta

The ECB provides funds and accepts deposits from business banks

in the Euro location, consisting of Malta, instead of straight from

people and businesses. Nonetheless, the rate of interest used

by business banks usually relocate line with ECB rates. However,

to date, the boost in ECB rates has actually relatively had small effect

on the rate of interest used by regional banks.

As per the Central Bank of Malta’s (CBM) latest quarterly

evaluation, in September 2022 the typical deposit rate of interest stood

at 0.14%, and the typical loan rate of interest stood at 3.25%. While

there have actually considering that been some advancements, these have actually been mostly

restricted to greater deposit rate of interest specifically on brand-new term

accounts, the discontinuation of set rate of interest on brand-new home

loan items, and little boosts in loan interest margins, and

however, these actions have actually just been used by some banks.

Should commercial banks increase rates on overnight deposit

accounts – more commonly referred to as savings accounts, and

increase their loan base rate, consumers and businesses will be set

to experience much bigger differences in their disposable incomes

and cash flows.

Why haven’t interest rates in Malta increased yet?

Based on the audited financial statements for year ending 2021,

the average loan-to-deposit ratio for core banks3 in

Malta stood at 56.6%, while that for significant banks in the Euro

area amounted to 104.8%4. This means that generally

Maltese banks do not resort to borrowing from the ECB at the

current 3.0% MRO rate (Main Refinancing Operations), but rather

rely on their own customer deposit base, at the average deposit

interest rate of 0.14%, as at September 2022, mentioned earlier, to

fund their loan book. In turn, this arrangement allows banks to

retain the currently advantageous interest rates on their loan

products.

How long will interest rates remain unchanged in Malta?

While the average loan-to-deposit ratio for Maltese core banks

stands at 56.6%, the ratio for individual core banks ranged from

circa 40.0% to over 90.0%, based on audited financial statements

for year ending 2021. The banks with a higher loan-to-deposit ratio

will probably be under greater pressure to increase their deposit

interest rates so as to maintain, and possibly strengthen, their

deposit base.

Once deposit interest rates increase for general savings

accounts, banks will very likely increase their base rates in order

to safeguard bank profitability.

What happens if banks increase their interest rates on

loans?

Locally, home and business loans are generally sanctioned at a

fixed margin over a bank’s base rate. Each bank’s base rate

is set by the individual bank and may change at any time at that

bank’s discretion. On the other hand, the fixed margin

specified at sanctioning, cannot be altered for the entirety of the

loan’s term.

Let’s take the example of a loan with a bank sanctioned

at a fixed margin, of say 1.5% over the bank’s base rate, of

say 2.0%, corresponding to a final interest rate of 3.5%. While the

fixed margin of 1.5% will remain constant, the 2.0% in the previous

example can increase or decrease at the bank’s

discretion.

While banks can increase their interest rates exclusively by

increasing the margin on new loans, an increase in the banks’

base rates would impact all existing and new loans and overdrafts.

Amongst other, an increase in banks’ base rate would be

expected to have actually the following effects on repayments:

New home loans As per current CBM

directives5, the repayment-to-income on home loans

cannot exceed 40.0% at sanctioning stage and that repayment must be

based on a stressed interest rate of 1.5% over the actual final

interest rate. Higher rate of interest will increase repayments, thus

decreasing the maximum amount that customers’ can be

sanctioned. As an example, in the event of an increase in interest

rate of 1%, a prospective 32-year old customer, with a maximum

permissible repayment of €1,000, would see their potential

loan amount decrease from roughly €250,000 to

€220,0006.

Existing home loans Increases in interest rates

will result in higher monthly repayments. The amount by which a

customer’s loan repayment will increase will depend on the

outstanding balance of the loan and the remaining term. As an

indication, an increase of 1.0% in the base rate on a loan with an

outstanding capital of €100,000 and a remaining term of 20

years, would imply an increase in repayment of circa €50 per

month, over the term of the loan7.

Personal loans Similarly to home loans,

increases in interest rates will impact the amount that can be

sanctioned and increase the monthly repayments. However, the CBM

does not stipulate a maximum repayment-to-income for personal

loans.

Business loans Increases in interest rates will

be reflected in higher loan repayments impacting the cash flow of

the business. Unlike home loans, repayment amounts on business

loans are not subject to a maximum by the CBM. For instance, if

interest rates were to increase by 1%, a business loan of

€500,000 with a term of 10 years, would incur an increase in

repayment of circa €240 monthly over the term of the

loan8.

Overdrafts Interest rates on overdraft is

charged periodically and there is no fixed monthly repayment with

respect to the outstanding balance. Therefore, increases in

interest rates will increase the interest due accordingly.

In summary…

If, when, and how to increase interest rates, will probably be

the single most important decision for local banks this monetary

year. What each bank decides will be influenced by their current

position in the market and will necessitate a fine balancing act

between the interests of their net deposit customers, their net

borrowing customers, and their shareholders.

On a reassuring note, the Maltese banking sector has undergone

significant expansion over the past two decades and today’s

banks are heterogenous and cater for different markets –

banks vary both in terms of balance sheet characteristics, as well

as market objectives. Thus, it is unlikely that all banks will

increase interest rates in unison, allowing customers to make the

best choices depending on their own personal realities.

Footnotes

1. Eurostat

2. National Statistics Office – Harmonised

Index of Consumer Prices (HICP): January 2023

030/2023

3. The Central Bank of Malta classifies APS, BNF,

BOV, HSBC, Lombard, and MeDirect Bank (Malta) as core domestic

banks.

4. European Central Bank – Supervisory Banking

Statistics, Third Quarter 2022

5. Central Bank of Malta – Directive no

16

6. Based on an increase in the loan interest rate

from 2.94% to 3.94%, 2.94% being the typical loan interest rate for

households as at September 2022 (CBM Quarterly Review

2023:1)

7. As above

8. Based on an increase in the loan interest rate

from 3.82% to 4.82%, 3.82% being the typical loan rate of interest for

non-monetary-corporations as at September 2022 (CBM Quarterly

Review 2023:1)

The content of this article is intended to provide a basic

guide to the subject. Specialist suggestions must be looked for

about your particular situations.

{kind=link}