This post is the latest part of the feet’s Financial Literacy and Inclusion Campaign

Russell Anderson is a man who has actually discovered to live within his simple methods. After a persistent disease required him to retire as a coach driver 3 years earlier, he handled to extend his advantages to cover his costs, consisting of lease and fuel.

Increasingly, he has actually discovered that stabilizing act more difficult to manage. Anderson, who resides in rural Scotland, says the rising cost of fuel has actually made it too costly to drive to his closest Aldi, the low-cost grocery store he can manage, suggesting he needs to take a circuitous bus trip rather.

When his cat fell ill suddenly, there were more costs to pay. “I went to the vets, spent £170, and he came back even more sick,” says Anderson. He had absolutely nothing delegated cover the costs that would have guaranteed the appropriate handling of his animal’s remains after it was put down.

Anderson’s credit ranking suggested he was rejected by 2 industrial loan providers. By possibility, he saw an advert for Glasgow-based neighborhood lending institution Scotcash on tv and, to his relief, was authorized for a £100 loan. He is deeply pleased. “They bent over backwards to help me,” he says. “I’ve not got a lot of debt, and I don’t need to borrow a lot of money, but no one else would lend.”

His story is one example of the precarity now being dealt with by individuals on low earnings throughout the UK. With the increasing cost of living extending budget plans to their outright capability, a single modification in scenario — from completion of a relationship, a damaged device or the death of a family pet — can be enough to press a household to breaking point.

Those with poor credit have couple of choices when they require a little loan. One lifeline is neighborhood loan providers, a little number of non-profits who support those dealing with monetary exemption from traditional financing. But the sector is having a hard time to accommodate the growing need. Compared with industrial loan providers, their financing pot is considerably smaller sized; they likewise follow requirements on cost for loans, which a growing variety of clients are not able to satisfy.

“I would say we decline 90 per cent of applicants and that really troubles me,” says Simon Dukes, president at not-for-profit loans supplier Fair for You. “It’s harder now for us to find people to say ‘yes’ to as a responsible lender.”

Those operating in the sector state that they urgently require more assistance to continue running, not to mention to scale up and match the requirements of a growing susceptible population. Many fear what will occur this winter season, with the Bank of England caution of an economic downturn and the most significant fall in household earnings for more than 60 years as the cost of energy and daily food products skyrockets.

“Regulation, funding and collaboration are super important because it’s such a precarious sector,” says Sharon MacPherson, president at Scotcash. “Think about how many businesses went bust during the pandemic: the future is never guaranteed.”

For those turned away by non-profits, the options can bring more danger. Buy now, pay later on items have actually dealt with examination over the stringency of their cost checks and the extremely last hope — prohibited financing by shylock — unlocks to exploitation.

With the MOT on his car due for renewal and a greater energy costs looming, Anderson expects he will require to rely on Scotcash once again prior to completion of the year to keep his car on the roadway.

The worst is yet to come

The history of not-for-profit loan providers, consisting of cooperative credit union and neighborhood advancement financing organizations, or CDFIs, go back to the late 20th century, driven by social motions in the UK and worldwide.

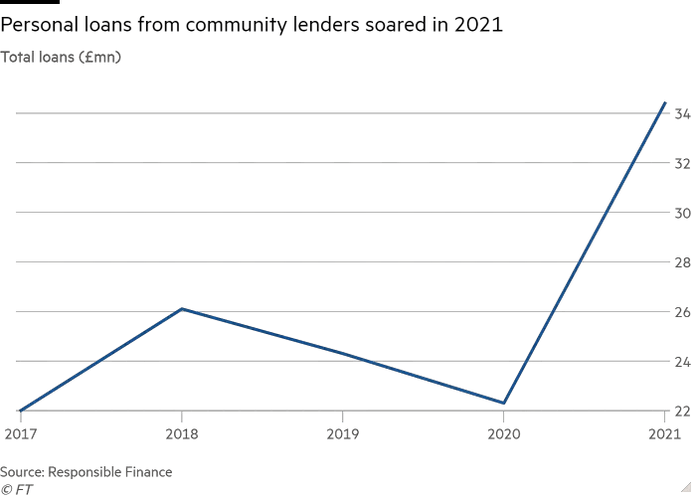

These community-focused loan providers are moneyed by a range of sources, varying from grants to banks. Figures from Responsible Finance, the sector’s trade body, revealed it had actually paid £228mn in all kinds of loans in 2021 — a 32 percent boost on the year prior to.

Faisel Rahman established east London-based Fair Finance in 2005, motivated by his experience operating in microfinance in Bangladesh, where it helped in reducing hardship. “Everything true about financial exclusion in Bangladesh is the same in London,” he says. “You need data to assess it effectively and you have to be flexible, responsive and personable.”

Rahman has actually discovered that the type of client requesting loans has actually altered gradually. Between 2005 and 2010, it was mainly those getting advantages. By 2015, the dominant group were those with variable earnings, consisting of gig economy employees and those on zero-hours agreements. Many typically have less than £50 at the end of monthly.

While a big percentage of clients reside in denied locations and have an average earnings of £15,000, Rahman stresses this is not universal. A consumer making £65,000 relied on Fair Finance to help settle payday advances after a missed out on payment.

The complete effect of the cost of living crisis is yet to emerge, says Rahman. In the UK, inflation struck a 40-year high of 9.4 percent in June, with the Bank of England forecasting it will peak at 13 percent by the end of the year, rising rates even more. Fair Finance’s analysis recommends that later on this year some clients will be not able to cover their costs and will have an unfavorable budget plan even with recommendations on how to handle their money.

Maggie, another Scotcash client, saw her food costs rise when her fridge-freezer broke in April, requiring her to shop everyday and spend more total. She discovered Scotcash through her regional authority in 2018, and they provided £500 to support her. Maggie, who experiences severe health conditions that limit her movement, has actually taken periodic loans from the lending institution ever since.

The issue is worsened by what advocates and neighborhood loan providers call the “poverty premium”. MacPherson says the most susceptible typically pay more for fuel since of pre-paid meters, or cannot manage insurance coverage. A number do not have their own checking account or cost savings. “They have no leeway whatsoever for putting money away,” she says. “Adding £2 or £3 extra on to a prepayment card for fuel means not being able to save it.”

Those who rely on neighborhood loan providers are likewise least most likely to access the growing variety of apps created to help clients make their money go even more such as budgeting tools.

“In our experience, customers are slow adopters of these products,” says MacPherson. “When you have very little money and anything could tip you over the edge, you want to protect that as much as you can.” For those who cannot access loans, non-profit loan providers play a crucial function in supplying monetary recommendations, she included, consisting of by using a digital advantages checker: “75 per cent of people are not claiming the benefits which they are entitled to,” she says. “It’s a double whammy alongside the increased cost of living.”

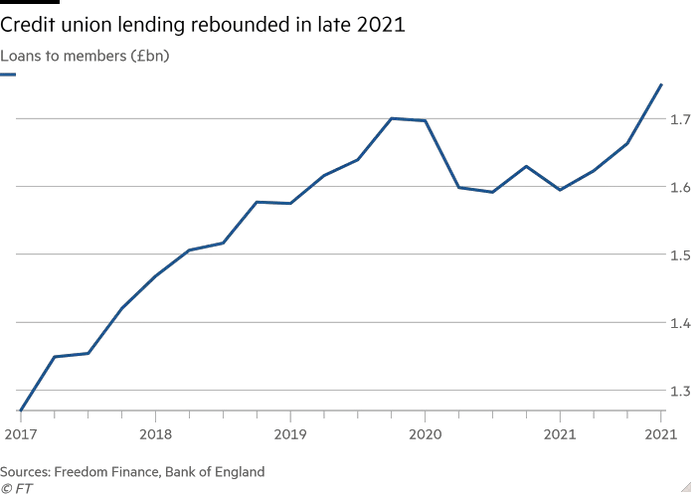

Credit unions, which count on deposits from members’ conserving accounts to make loans and have a cap of about 43 percent APR set by the federal government, are likewise dealing with an uptick in need.

In May, digital financing market Freedom Finance said that a record 1.9mn individuals in the UK were now members of cooperative credit union with overall loans to members by the end of 2021 reaching £1.74bn, another all-time high. But their financing is topped by the amount of deposits they hold.

“The credit union movement in the UK is very small compared with the US,” says Robin Fieth, president of the Building Societies Association, which represents a variety of cooperative credit union. “They have limited capacity to be the solution.” BSA members had actually cautioned him that it would just show harder in winter season, when heating up need is far greater.

The significance of non-profit loan providers has actually grown as industrial opportunities have actually diminished. In current years, the Financial Conduct Authority secured down on so-called “non-standard finance providers” that grew after the 2008 monetary crisis however drew criticism for their high charges.

Maggie says she has actually utilized Provident Financial, previously the UK’s biggest doorstep lending institution (which offer loans and gather payments from a client’s home), however wound up paying back almost double the quantity she obtained. Provident shuttered its customer credit system in 2015.

The variety of active high-cost, short-term loan providers in the UK fell by almost one-third in between 2016 and the 3rd quarter of 2020, according to the FCA’s figures.

“We know supply in the market has lessened because we’ve seen increased scrutiny and a number of lenders with poorly designed products being challenged which is, frankly, a good thing,” says Brian Brodie, chairman of Freedom Finance. “The unintended consequence is that fewer people are able to access finance.”

Loan sharks

One difficulty throughout the sector stays a patronising and typically moralistic mindset towards those without best credit rating, state specialists operating in the sector. While individuals on greater earnings can access overdrafts or charge card with competitive rates to much better handle their money when times are difficult, those living hand to mouth have no such safeguard.

“Customers are financially savvy — there’s a common problem of people equating income with intelligence,” says Rahman. “They don’t need to be told how to do things, they need a fair option.”

Charities have actually cautioned that buy now, pay later on is becoming one location of issue. Providers of the short-term credit have actually dealt with concerns around how completely they examine a user’s capability to manage loans, with issues that users can pack up financial obligation throughout numerous companies. “Out of every 10 people we see, five or six are using buy now, pay later,” says MacPherson. “We’ve seen an explosion in that type of product, both for retail users but also daily needs, which is really unsustainable.”

While the federal government has actually devoted to managing the sector, it is just anticipating to present brand-new laws by the middle of 2023. After that, the FCA would need to seek advice from on guidelines.

More troubling is that a growing variety of homes are susceptible to shylock or prohibited loan providers. The figure has actually increased from 310,000 in 2010 to 1.08mn in 2022, says Cath Williams, a supervisor in the federal government’s England Illegal Money Lending Team.

“The main reason people turn to them has always been everyday expenses — historically that’s been washing machines and school uniforms,” says Williams. “But more and more people are saying it’s to put food on the table or pay the electricity meter.”

In lots of cases, victims think they are obtaining from a friend, says Williams, till they’re not able to satisfy their payments. And shylock are getting more tech savvy with their approaches of intimidation. “One illegal money lender who was prosecuted last year was using altered Snapchat pictures, with the implication that they could come around and knock on victims’ doors,” she says.

For those impacted, leaving the clutches of an unlawful money lending institution takes some time. “The whole journey of realising that this isn’t a friend, then realising that this is something they need help to get out of — realising that it’s a loan shark — and then making a phone call to us is a three-year process,” she says.

Williams, whose group works carefully with cooperative credit union, says they cannot deal with need and the numbers they turn away are increasing. “As that goes up, there is a concern in terms of where people go — sometimes it’s family and friends . . . but at some point down the line they might turn to illegal money lenders, maybe as fuel prices go up.”

Case for financial investment

There is no single service to safeguarding the non-profit financing sector, however loan providers concur that making sure a higher quantity of money is available is a primary step. One path is the inactive possessions fund, a pot worth £880mn from monetary possessions consisting of checking account, pension plans and securities that have actually been unblemished for an extended period.

These possessions, administered by the Department for Digital, Culture, Media and Sport, are presently being invested in monetary addition, along with social financial investment and youth tasks, with a variety of neighborhood loan providers taking advantage of the task. In July, the federal government released an assessment into what triggers need to be moneyed.

Dukes says Fair for You has actually had the ability to “grow its social impact significantly” thanks to Dormant Assets financing in 2020. “The current cost of living crisis makes the case for investment in financial inclusion even more pressing,” he says. Theodora Hadjimichael, president of Responsible Finance, echoed Dukes’ belief, while highlighting the variation in financing in between fintechs and the non-profit sector.

“If you look at how much has been invested into buy now, pay later, and how much has been invested into high-cost commercial lenders, it’s eye-watering compared with CDFIs,” she says. “The more the government prioritises financial inclusion for dormant assets, the better.”

MacPherson likewise required more regional authorities to get included. Scotcash is moneyed by Glasgow City Council and Glasgow Housing Association, now Wheatley Homes Glasgow. “It can be really hard to keep ahead of the curve of fintechs and ensuring that you’re relevant to customers,” she says. “We absolutely need government to build capacity of the sector.”

Tulip Siddiq, shadow financial secretary to the Treasury, says the Labour celebration would look for to reform legislation around the sector if chosen. “Labour has pledged to double the size of the co-operative and mutual sector,” she says. “This will require regulators, such as the FCA and Prudential Regulation Authority, to have an explicit remit to report on how they have considered specific business models, such as mutuals, whose needs are too often ignored.”

The Treasury says it is supporting homes with a £37bn package, consisting of a direct payment of £1,200 to 8mn of the most susceptible households. “We’re also backing Fair4All Finance with almost £100mn of government funding this year — a record amount — to support their work on financial inclusion, including helping people to access affordable credit,” it says.

Rahman says legislation to motivate mainstream loan providers to support regional neighborhoods would make a favorable distinction. In 1977, the United States enacted the Community Reinvestment Act to make sure that banks made loans in areas where they took deposits. “We don’t need the same [legislation as the US] but it’s crazy that there is no obligation for banks to be involved in tackling exclusion or accountable to the communities they are in,” he says.

“If you believe that financial exclusion is a problem, you have to believe that there’s a better way of doing this.”

Letter in reaction to this post:

Charities require very same loan gain access to as little businesses / From Sarah Gordon and others

{kind=link}